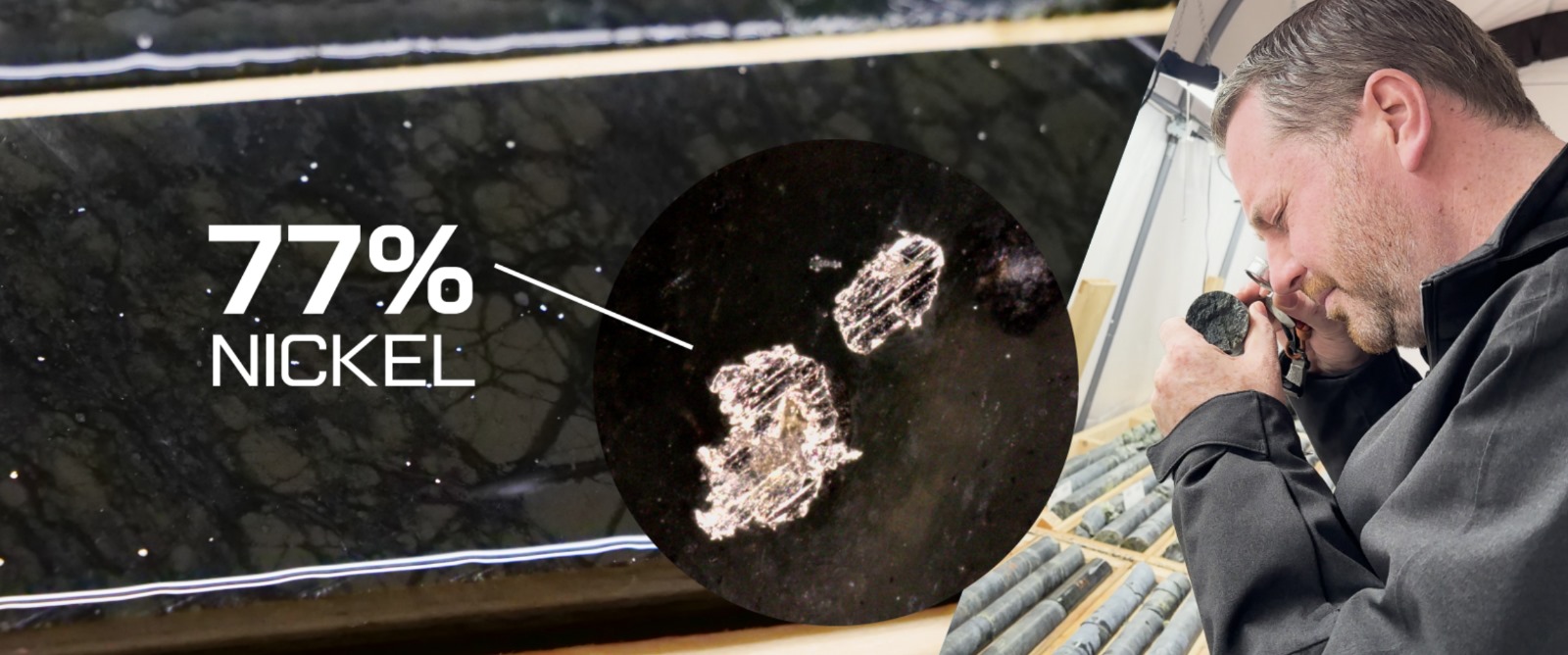

First Atlantic Nickel & Cobalt Corp. (TSX-V: FAN | OTCQB: FANCF) has discovered a rare magnetic nickel-cobalt alloy in Newfoundland containing 77% nickel[1] that can bypass the midstream smelting bottleneck and ship directly downstream into North American EV battery refineries, stainless steel, aerospace, and defense industries.[2]

Western economies are electrifying. Defense, aerospace, EVs, robotics, and advanced manufacturing all run on nickel and cobalt. China has spent the last 13 years building the supply chain to deliver them.

China produces roughly 10% of the world’s nickel, cobalt, copper, and lithium. It controls 65–90% of global processing for each.[9]

The groundwork was laid in 2012, when Hong Kong Exchanges acquired the London Metal Exchange[10] — giving Beijing indirect influence over global nickel and cobalt pricing. A year later, China launched the Belt and Road Initiative and began securing critical mineral mining and processing across Asia, Africa, and South America. State-backed companies poured an estimated $65 billion into Indonesian nickel alone.[11]

The scale has only grown. Cumulative BRI engagement has now reached $1.4 trillion across 150 countries, and in 2025, 61% of China’s record metals and mining spending flowed directly into processing facilities like smelters and refineries.[12] Beijing isn’t just buying minerals. It’s buying the midstream.

The West doesn’t control the critical minerals supply chain behind its consumer electronics, EV batteries, or defense systems. China does, and has for over a decade.

“There is no adequate alternative supply of nickel produced outside of China or by non-Chinese companies.”[9]

— Center for Strategic and International Studies, 2025

The pressure isn’t slowing. The IMF projects that real prices for nickel, cobalt, and lithium could rise by several hundred percent from 2020 levels, with accumulated production value through 2040 reaching $4.1 trillion for nickel and $1.6 trillion for cobalt.[3]

“Even if the U.S. and EU were to dig more minerals out of the ground, many of these minerals would need to be shipped overseas for concentrating, refining, and smelting without significant increases in U.S. and European mineral refining and smelting capacity.”[13]

— Brookings Institution, 2022

The race to onshore is already underway. The infrastructure to win it isn’t built.

Conventional nickel processing is energy-intensive, capital-heavy, and environmentally destructive — and China owns or controls most of it.[9] North America hasn’t built a new nickel smelter in decades.[4]

The United States has zero operating nickel smelters.[4] Its only domestic nickel mine, the Eagle Mine in Michigan’s Upper Peninsula, accounts for less than 5% of national consumption and is approaching the end of its reserves.[14] Most remaining U.S. nickel and cobalt reserves sit in Michigan and Minnesota — including the Twin Metals project, which holds an estimated 95% of U.S. nickel reserves but has been tied up in courts and litigation for nearly two decades without mining a single ounce of ore.[15] Canada has two aging nickel smelters left in Sudbury running near capacity,[5][4] with rising electricity costs and tighter environmental regulations squeezing what’s left of the continent’s processing capacity.

Washington is trying to backstop the gap, but progress is slow. A proposed $7.4 billion Korea Zinc smelter in Tennessee was announced in December 2025, but less than $1.5 billion has been committed — all from the U.S. government, split between the Department of Defense and the Department of Commerce.[16] The project isn’t permitted, isn’t fully funded, and isn’t built. And on its own schedule, it would process zinc, lead, and copper. Not nickel.

“Even where the United States has domestic mining capacity, such as for cobalt, nickel, and rare earth elements, the United States lacks the domestic processing capacity to avoid downstream net-import reliance.”[16]

— The White House, June 2021

Building new capacity is harder than the headlines make it look. A single smelter draws power on the scale of a mid-sized city, and new U.S. smelter projects are competing for that power against AI data centers willing to pay double. Century Aluminum announced a $5 billion U.S. smelter in March 2024 and, more than a year later, still hasn’t picked a site — it can’t lock down a long-term power contract at a price that makes the project work.[17] The last generation of Western nickel projects fared no better: BHP poured roughly US$3 billion into its Western Australia nickel division before suspending its Kalgoorlie smelter, Kwinana refinery, and Mt Keith and Leinster mines in 2024, writing down US$3.5 billion in the process.[18] Ravensthorpe — opened in 2008 after massive cost blowouts — has been shut down three times in 17 years.[19]

“As the Eagle Mine looks at closure, the United States either will have to find new nickel to mine or import all nickel for production, which may have economic and security implications.”[14]

— U.S. Federal Reserve Bank, December 2025

For most of the past three years, Indonesian nickel flooded global markets and depressed prices. That’s reversing. In late 2025, Indonesia cut 2026 nickel mining quotas by more than 30%, added new royalties, and pushed ore prices higher.[20] A sulfur-supply shock tied to the Iran war drove sulfuric acid costs sharply higher for the Chinese-operated HPAL plants that dominate Indonesian processing, forcing several to cut output.[21] The 2025 global nickel surplus has flipped to a projected 2026 deficit.[22]

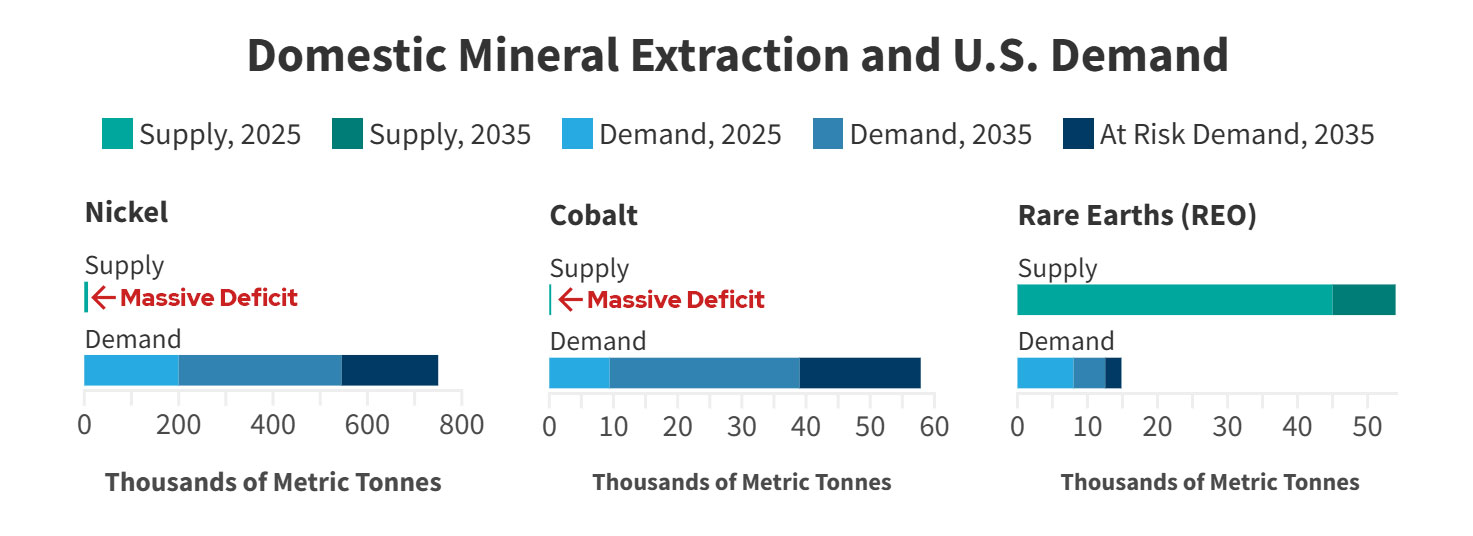

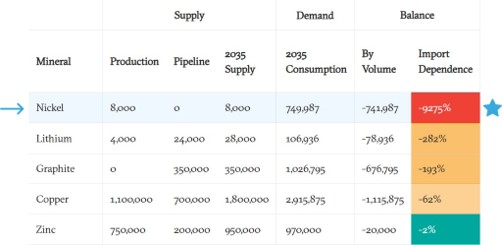

Demand is moving the other way. The Carnegie Endowment estimates U.S. nickel consumption will reach roughly 742,000 tonnes per year by 2035 — about 93 times what the United States produces today — requiring an estimated 17 new mines just to close the domestic gap.[8] The IEA projects roughly 60 new nickel mines globally by 2030, with consumption set to roughly quadruple by 2040. The IMF projects total accumulated production value from 2021–2040 of $4.1 trillion for nickel and $1.6 trillion for cobalt.[3]

Prices have already moved. Nickel rallied from roughly $6.35/lb at its 2025 low to a recent two-year high near $8.89/lb in May 2026 — a 40% move.[6] Cobalt rose from $16.62/lb in May 2025 to roughly $25.53/lb by late April 2026 — a 54% move, driven by DRC export quotas and tightening supply.[7]

According to Carnegie Endowment for International Peace in November 2025, by the year 2035, projected U.S. nickel demand will exceed projected mined supply by 9,275%, the largest import-dependence gap of any critical mineral.[8]

Canada doesn’t fill the gap as it mines and ships. RBC’s February 2026 Mine & Refine report laid it out: most of the critical minerals mined in Canada are exported for processing, primarily to China.[23] CIBC put numbers on what fixing that would actually require:

“We’re the fifth largest nickel producer in the world, and the World Bank forecasts a doubling of global nickel demand by 2050. So if we look at what that means for Canada in the next twenty-nine years, we’ll need to see seven new nickel mines come online to new nickel smelters and a nickel refinery just to maintain current global market share. That’s just one material, and we’re not talking about expanding market share. We’re talking about just maintaining it.”[24]

— CIBC

The processing gap isn’t just an economic problem.

“The real strategic vulnerability today is not our geology; it is our processing capacity and supply chain dependence.”[25]

— Dr. Nadia Mykytczuk, Executive Director, Goodman School of Mines, Laurentian University. Testimony to the House of Commons Standing Committee on National Defence.

Demand is rising. Supply and processing aren’t keeping up.

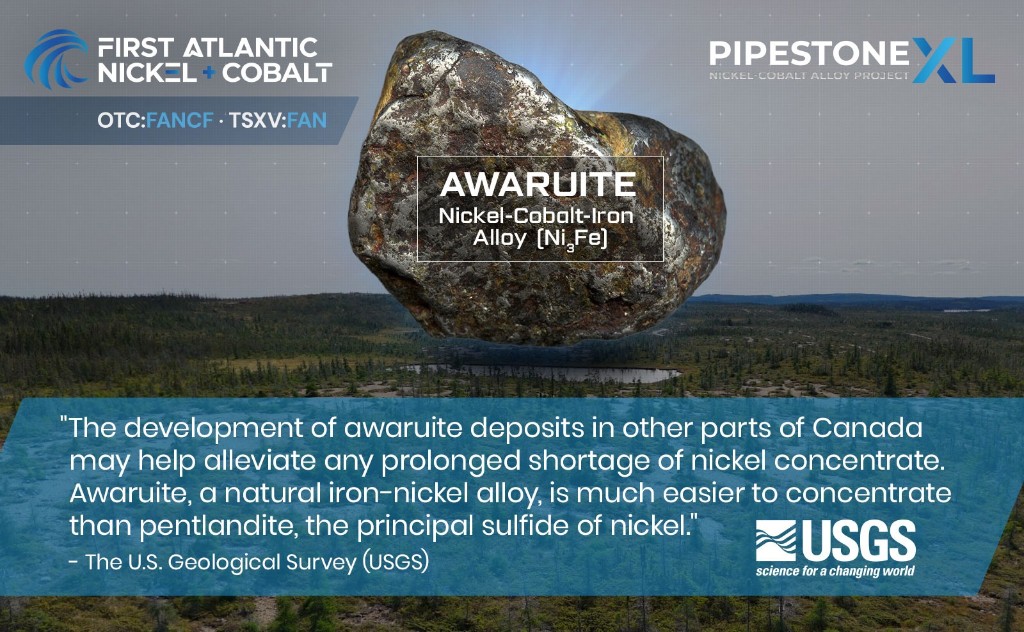

Awaruite (Ni3Fe) is one of the highest-grade nickel minerals on Earth and the only one that occurs naturally as a magnetic metal alloy. It’s the product of serpentinization — a geological process in which hydrogen generated from altering ultramafic rock reduces nickel and iron into native metallic form.[2]

That matters because conventional nickel sulfide and laterite ores are chemically bound to sulfur, magnesium, and silica — and require capital-heavy, energy-intensive, environmentally high-impact secondary midstream processing like smelting or high-pressure acid leaching to break those bonds, reduce the nickel to metal, and convert it into a concentrate suitable for downstream refining. Awaruite is already pre-reduced: it leaves the ground as a metal alloy, with no chemical bonds to break.

Awaruite has no chemical bonds to break. It’s already metallic, naturally magnetic, and sulfur-free. That means avoiding the cost and environmental burden of secondary midstream processing — the high electricity consumption and SO2 emissions of smelting, the sulfuric acid intensity and toxic tailings of HPAL, and the treatment and refining charges (TCs/RCs) producers pay third-party smelters to take their concentrate.[2]

At the RPM Zone of Pipestone XL, electron microprobe analysis by SGS Canada confirmed awaruite averaging 77.62% nickel and 1.69% cobalt, with peaks up to 86.68% nickel and 6.05% cobalt, and chromite grading 60.2% Cr2O3 identified as a potential co-product.[26]

Awaruite can be concentrated through magnetic separation and flotation — well-established processing methods — into a high-grade nickel-cobalt concentrate of greater than 60% nickel that can be shipped directly downstream into stainless steel, EV battery, and specialty alloy industries, bypassing midstream smelting.[2]

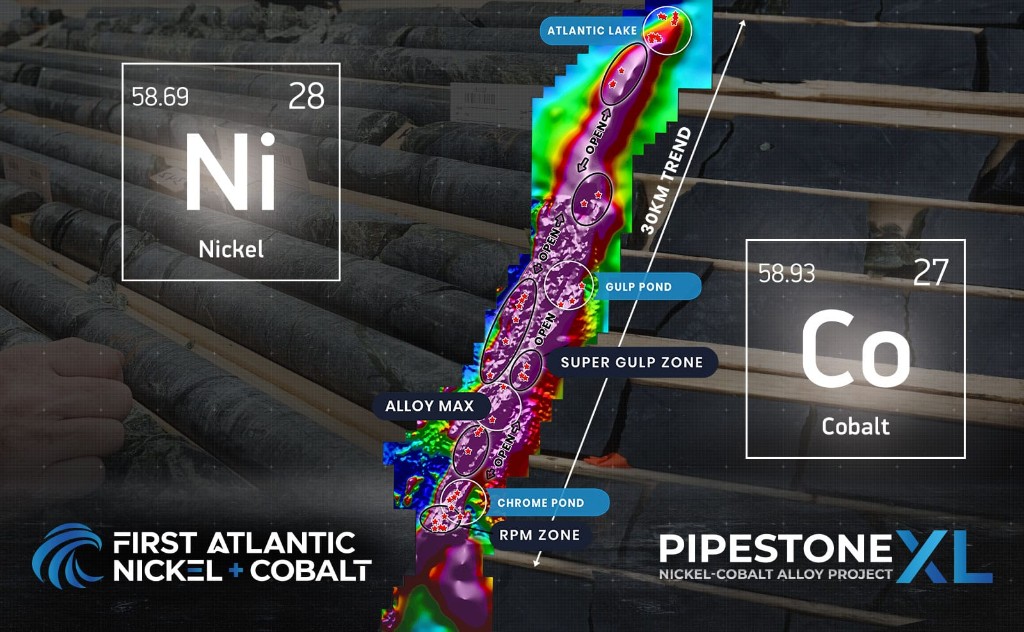

First Atlantic Nickel & Cobalt Corp. (TSX-V: FAN | OTCQB: FANCF) holds 100% of an entire 30-kilometer ophiolite district in Newfoundland. The Pipestone XL Nickel-Cobalt Alloy Project is the largest nickel-cobalt and chromium discovery in the Atlantic in 30 years.

The geology is a 489-million-year-old ophiolite of ancient ocean crust, and mantle thrust onto land along the Appalachian Orogen. The entire 30-kilometer belt is enriched in nickel, cobalt, and chromium through serpentinization, a natural process that releases nickel from the rocks and forms a nickel-cobalt alloy.

Drilling has confirmed nickel-cobalt alloy mineralization over 1.2 km by 800 m, with intercepts up to 447 meters. Magnetic concentrates run up to 2.35% nickel and 8.17% chromium.

Announced March 2026. Located 7 km north of RPM, with an initial 4 km by 1.2 km target area, roughly four times RPM’s footprint. Early geophysics suggests it may be larger still.

A system this size could support multiple large open pits within a single geological system. That’s the kind of scale that defines a major mining district.

Most North American mining projects get held up by a lack of infrastructure — no access to midstream smelting, no grid power, or no proximity to roads. Pipestone XL doesn’t have those problems. Awaruite skips midstream smelting entirely, and the site is road-accessible to the Trans-Canada Highway, sits within roughly 10 km of a clean hydroelectric dam, and has additional high-voltage transmission lines nearby.

Newfoundland is one of the few places in North America where a new mine can actually reach production on a fast timeline. Hydroelectric power is cheap and abundant, permits move quickly, and deep-sea Atlantic port access opens direct shipping to U.S. and European manufacturers.[27]

The province hosts 31 of the 46 minerals identified as critical by the United States, EU, Japan, Australia, UK, and South Korea — and it ranks among the world’s top mining jurisdictions year after year on the Fraser Institute’s Annual Survey.[27]

Equinox Gold’s Valentine Gold Mine — about 80 km from First Atlantic’s Pipestone XL Project — proves the point. The project description was filed with provincial and federal regulators in April 2019. Provincial environmental approval came in March 2022 (under three years), federal approval in August 2022, and the mine poured first gold on September 14, 2025 — declaring commercial production in November.[28][29] Once fully ramped, Valentine will be the largest gold mine in Atlantic Canada.

By comparison, Ontario’s Ring of Fire — discovered in 2007 with an estimated $60 billion in critical minerals[30] — still has no road, no grid power, no rail, unresolved First Nations land rights, no smelter, and no shovel in the ground after almost two decades.

The last major nickel-cobalt discovery in Newfoundland was Voisey’s Bay. It was acquired in 1996 for $4.3 billion, with shares up 20-fold going into the deal.[31] In today’s dollars, that’s more than $8 billion. In 2022, Tesla signed a supply agreement with Vale to secure Voisey’s Bay nickel for its North American gigafactories.[32]

PIPESTONE XL COULD BE THE MOST STRATEGIC NICKEL, COBALT AND CHROMIUM DISCOVERY IN THE WESTERN HEMISPHERE.

The West cannot build its way out of the midstream bottleneck on a useful timeline. New smelters cost billions, take a decade to permit, and compete with AI data centers for power. Mining alone doesn’t solve it. Buying back Indonesian or Congolese supply doesn’t solve it. The only durable answer is a nickel-cobalt source that doesn’t need a smelter in the first place.

That source exists. It is awaruite, a naturally magnetic 77% nickel-cobalt alloy. First Atlantic Nickel & Cobalt Corp. (TSX-V: FAN | OTCQB: FANCF) has drilled the first major awaruite discovery since the USGS flagged it as a strategic solution in 2012 — a 30-kilometer district in Newfoundland, 100% Company-controlled, road-accessible, powered by hydroelectricity, and 80 km from the most recently permitted gold mine in Atlantic Canada.

What you’re looking at:

The midstream bottleneck is the binding constraint on Western critical minerals. Awaruite is the only primary nickel mineral that goes around it.

Our White Paper on Onshoring the North American Nickel-Cobalt Supply Chain

Now available — enter your email and we’ll send it to you instantly.

First Atlantic Nickel Corp. (TSXV: FAN) (OTCQB: FANCF) (FSE: P210) is a Canadian mineral exploration company developing the 100%-owned Atlantic Nickel Project, a large-scale nickel project strategically located near existing infrastructure in Newfoundland, Canada. The Project’s nickel occurs as awaruite, a natural nickel-iron alloy containing approximately 75% nickel with no-sulfur and no-sulfides.

CEO & Director

Strategic Advisor

Over 25 years of leadership across critical minerals processing, advanced materials, and energy research. Former Program Director at the U.S. Department of Energy, where he designed and led ARPA-E's MINER critical minerals program and geologic hydrogen portfolio, including the first U.S. federal program to competitively fund stimulated geologic hydrogen research.

Dr. Wicks serves as Strategic Director, ASCENT Japan at Renaissance Philanthropy and sits on the Advisory Board of the Chimaera Fund, a U.S. geologic hydrogen initiative awarded a contract by the U.S. Department of the Air Force.

Senior Strategic Advisor

Gary Stanley is former Director of the Office of Critical Minerals and Metals at the U.S. Department of Commerce. He has 40+ years experience serving under every U.S. President from Ronald Reagan to Joe Biden. Mr. Stanley worked with both public and private sector stakeholders to strengthen American supply chains and U.S. global competitiveness in critical minerals. He was lead author of the 2019 US Federal Critical Minerals Strategy.

Project Geologist

22 years of mining and exploration experience ranging from grassroots exploration to major mining projects. Beginning in the prolific Red Lake gold district in Ontario, his career spans nickel, gold, diamonds, and antimony including the Valentine Lake & Voisey’s Bay projects in Newfoundland & Labrador.

Mike completed his undergraduate honours thesis in 2012 at Memorial University of Newfoundland examining the formation of awaruite nickel-iron alloy at the Atlantic Lake region of Pipestone Pond Ophiolite Complex.

Director

Brings over 20 years of finance and capital market experience. Former investment advisor at Mackie Research, Jordan Capital Markets, and Canaccord Capital Corp. Has been responsible for raising tens of millions of dollars in equity financing. Significant experience specializing in developing, restructuring and financing venture capital companies.

Independent Director

CFO

Head of Investor Relations

Rob Guzman is the Founder & Managing Partner of Xander Capital Partners. Xander has over 30 years of deep experience in the financial sector, corporate development, and investor relations. Based in Orlando, Florida, Rob commands an extensive cross-border outreach network that seamlessly connects high-growth public companies with global capital markets. Throughout his distinguished career, Rob has specialized in scaling public entities from inception to high-value exits. Most notably, he served as the Head of Investor Relations for Alpha Lithium Corp., from its 2019 launch through to its landmark $300-million-plus buyout in 2023. Rob delivers bespoke investor relations solutions and strategic frameworks engineered to elevate corporate profiles, accelerate market visibility, and unlock long-term shareholder value.

1890 – 1075 West Georgia Street, Vancouver, British Columbia, V6E 3C9, Canada

This webpage has been prepared and distributed by First Atlantic Nickel & Cobalt Corp. and constitutes a promotional communication. It is provided for informational purposes only and does not constitute financial or investment advice or a recommendation, offer or solicitation to buy or sell any securities. Investing in securities involves risk, including the risk of loss of principal. Past performance is not indicative of future results, and no assurance can be given that any objectives, projections or expectations described on this page will be achieved. Market forecasts cited on this page are third-party views and are inherently uncertain; actual price and demand outcomes may differ materially.

No securities regulator or stock exchange has reviewed or accepts responsibility for its contents. Recipients should conduct their own research and consult qualified investment professionals before making any investment decisions. By reading this communication, you acknowledge and agree that neither First Atlantic Nickel & Cobalt Corp. nor any of its directors, officers, employees, agents, or promoters accepts any liability for any direct or consequential loss or damages arising from reliance on the information contained herein.

The scientific and technical information on this page has been reviewed and approved by Adrian Smith, director and the Chief Executive Officer of the Company whom is a qualified person as defined by NI 43-101. The qualified person is a member in good standing of the Professional Engineers and Geoscientists Newfoundland and Labrador (PEGNL) and is a registered professional geoscientist (P.Geo.). Unless otherwise indicated, the technical information on this page is derived from the Company’s previously filed disclosure, including news releases available under the Company’s profile on SEDAR+.

This page contains “forward-looking information” within the meaning of applicable Canadian securities laws, including, without limitation, statements regarding: anticipated North American and U.S. demand for nickel, cobalt and chromium; projected supply deficits, import dependence and price trends; the potential strategic importance of the Pipestone XL Project; the potential for awaruite mineralization to support smelter-free or onshore processing; the potential ability of concentrate from the Project to be processed by downstream North American customers; expected metallurgical, recovery, concentrate grade, by-product and processing outcomes; the extent, scale and continuity of mineralization; future exploration, drilling, metallurgical testing and development plans; permitting, environmental, infrastructure and timeline advantages; and potential opportunities relating to chromium, geologic hydrogen and carbon capture. Forward-looking information is often, but not always, identified by words such as “expects,” “plans,” “targets,” “believes,” “projects,” “potential,” “could,” “may,” “will,” “anticipates,” and similar expressions.

Forward-looking information on this page is based on a number of material factors and assumptions, including, among other things: the accuracy of current geological, geophysical, geochemical, drilling, sampling, assay and metallurgical data interpretations; the continuation of observed mineralization and metallurgical characteristics; the ability to obtain results from additional drilling and testing consistent with results to date; the availability of financing, personnel, equipment and contractor support; the timely receipt of permits, approvals and access; the availability of infrastructure, processing, refining and transportation alternatives; the continuation of supportive critical mineral, trade and industrial policies in Canada and the United States; and management’s current expectations regarding market conditions, demand, pricing and supply chain dynamics for nickel, cobalt and chromium.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those expressed or implied by such forward-looking information. These include, without limitation: exploration results not supporting current interpretations; drilling, sampling, assay, metallurgical or recovery results that differ from results obtained to date; the absence of a mineral resource estimate or economic study demonstrating economic viability; changes in commodity prices, demand forecasts, tariffs, quotas, trade measures or critical mineral policies; the inability to secure financing, permits, social licence, infrastructure, contractors, processing arrangements or offtake relationships on acceptable terms or at all; technical, engineering, processing, scale-up or recovery challenges; cost inflation; environmental and regulatory risks; title, access, weather and operational risks; and general economic, market and capital markets conditions. Readers are cautioned that actual results may differ materially from the forward-looking information on this page, and undue reliance should not be placed on such information.

The forward-looking information on this page is made as of the date of publication of this page, and First Atlantic Nickel & Cobalt Corp. undertakes no obligation to update or revise such information except as required by applicable securities laws.

Readers should review the Company’s continuous disclosure filings available on SEDAR+ and should conduct their own independent review before making any investment decision.

Our White Paper on Onshoring the North American Nickel-Cobalt Supply Chain

Now available — enter your email and we’ll send it to you instantly.