TSX-V: FAN

OTCQB: FANCF

$FANCF

$FANCF  $FAN.V

$FAN.V

First Atlantic Nickel & Cobalt Corp. OTCQB: FANCF | TSX-V: FAN

As North America races to onshore critical mineral supply, First Atlantic Nickel & Cobalt's rare awaruite (Ni₃Fe) discovery is positioned to deliver a large-scale, smelter-free source of nickel and cobalt.

Key Takeaways

First Atlantic Nickel & Cobalt Corp. (OTC: FANCF | TSX-V: FAN) has drilled the first major awaruite discovery since the United States Geological Service (USGS) identified it as a solution to nickel shortages in 2012.

The Pipestone XL discovery of awaruite (Ni₃Fe), Earth's rarest naturally magnetic nickel-cobalt alloy, is the largest nickel-cobalt alloy and chromium discovery in the Atlantic in 30 years, since Voisey's Bay, which was acquired for $4.3 billion in 1996[1] (more than $8 billion adjusted for inflation).

Awaruite is a natural alloy of approximately 77% pure nickel with cobalt and iron, and can be processed using magnetic separation with no smelter required — bypassing the North American smelter bottleneck and enabling a fully onshore supply chain feeding directly into U.S. battery refineries, stainless steel, and defense manufacturing.

Nickel prices have risen 35% from their 2024 lows into early 2026 after Indonesia cut mining quotas by an estimated 11%, according to Goldman Sachs.[2] Cobalt prices have surged 170% from their 2024 lows after the DRC imposed export bans and quota restrictions. The market is already moving, and the IMF's long-term outlook is even more significant:

"The IMF projects that real prices of nickel, cobalt and lithium would rise several hundred percent from 2020 levels... total accumulated production value from 2021–2040 reaching $4.1 trillion for nickel, $1.6 trillion for cobalt — across all four critical energy transition metals, over $13 trillion, rivaling the total value of crude oil production."[4]

— International Monetary FundAs Washington pushes to onshore critical mineral processing and reshore advanced manufacturing, First Atlantic Nickel & Cobalt Corp. (OTCQB: FANCF | TSXV: FAN) is positioned to capitalize on the rapidly increasing demand for nickel and cobalt mined and processed outside of Chinese-controlled supply chains. The company's Pipestone XL awaruite discovery represents one of the most strategically significant critical mineral opportunities in North America: a smelter-free source of nickel and cobalt that can feed directly into U.S. refineries and battery manufacturers without touching Chinese-controlled processing infrastructure.

"Even where the United States has domestic mining capacity, such as for cobalt, nickel, and rare earth elements, the United States lacks the domestic processing capacity to avoid downstream net-import reliance."[5]

— White House, January 14, 2026

The United States holds less than 1% of global nickel reserves.[6] By 2035, nickel import reliance is projected to hit 9,275% — the highest of any critical mineral, according to the Carnegie Endowment for International Peace.[7]

China produces just 10% of the world's nickel, cobalt, copper, and lithium but controls 65–90% of global processing.[8] Much of that control is financed directly by the Chinese government, creating a dangerous reliance that the U.S. has yet to deal with.

Indonesia mines more than 60% of the global nickel supply. After it banned raw ore exports in 2020, Chinese state-backed companies invested an estimated $65 billion to gain near-total control of Indonesian processing. Indonesia's own parliament confirmed that China now controls 90% of the country's nickel industry[9].

"There is no adequate alternative supply of nickel produced outside of China or by non-Chinese companies."

— Center for Strategic and International Studies, 2025

According to the U.S. Army War College, the DRC produces 80% of the world's cobalt, Chinese state-owned enterprises control 80% of total output, and their refineries account for as much as 90% of global cobalt supply.[10]

In 2012, Hong Kong Exchanges purchased the London Metal Exchange,[11] giving Beijing indirect control over global nickel and cobalt pricing. A year later, China launched its Belt and Road Initiative, systematically securing critical mineral mining and refining across Asia, Africa, and South America. From consumer electronics to EV batteries to defense systems, the U.S. depends on a supply chain it doesn't control — and China is more than a decade ahead.

The U.S. Department of Defense has called nickel "an essential component of high-temperature alloys used in aerospace, as well as stainless steel and lithium-ion batteries." Yet Twin Metals in Minnesota, which holds approximately 95% of U.S. nickel reserves and 88% of U.S. cobalt reserves, remains blocked by a 20-year federal mining ban.[12] The U.S. has not mined chromium since 1962.[13]

Even if the U.S. could mine more nickel, there is nowhere to process it. Building a new nickel smelter could cost billions and require billions more in electrical capacity to power it, while facing lengthy permitting, EPA regulations over toxic SO₂ emissions and acid mine drainage, and fierce community opposition.

North America lost one of its three nickel smelters in 2018.[14] The two remaining are in Canada,[15] both near capacity and under pressure from stricter environmental regulations and rising electricity costs. No new nickel smelters have been built in North America in decades.

"Nickel continues to grow in importance as a strategic resource... the United States either will have to find new nickel to mine or import all nickel for production, which may have economic and security implications."[16]

— U.S. Federal Reserve Bank, December 2025

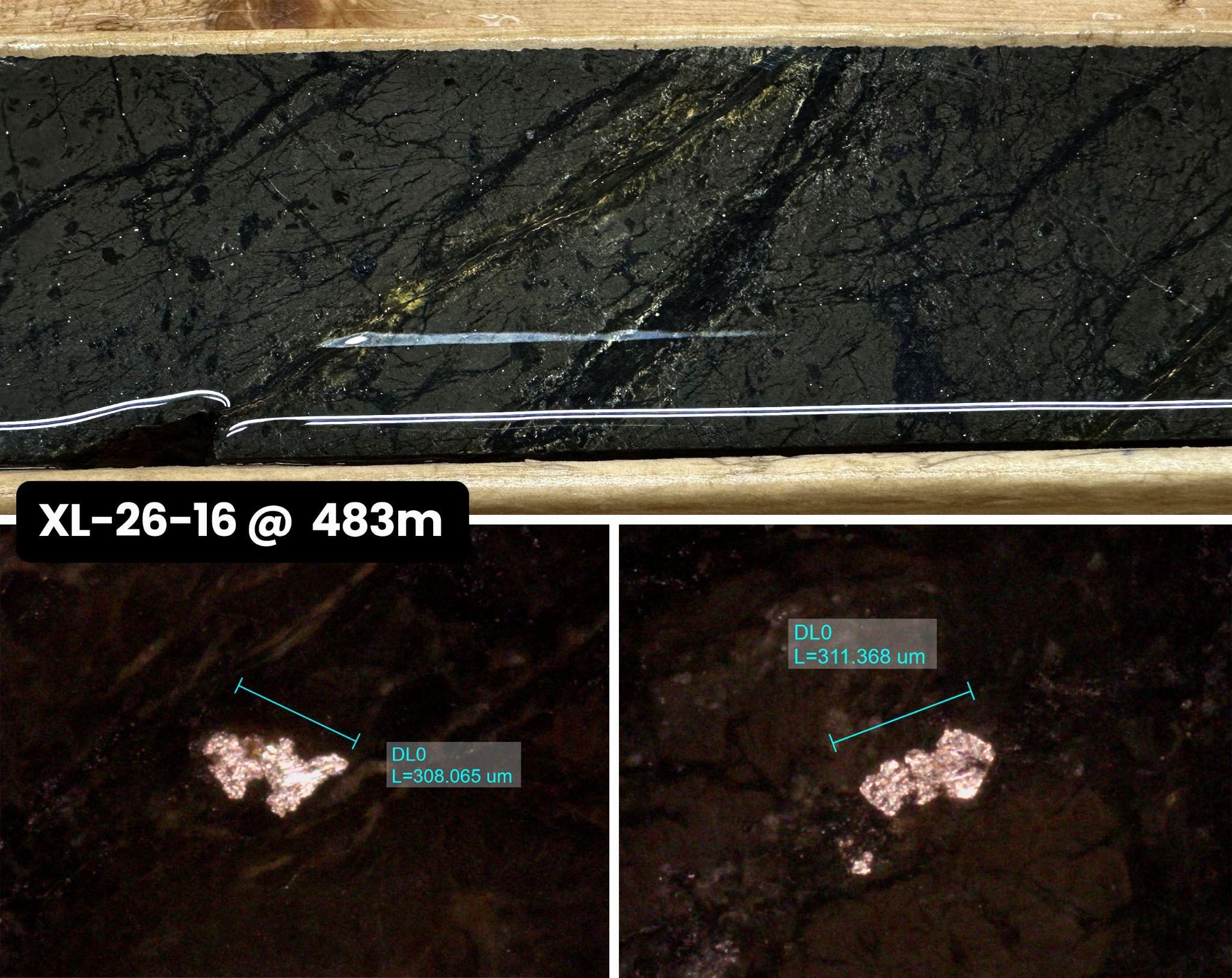

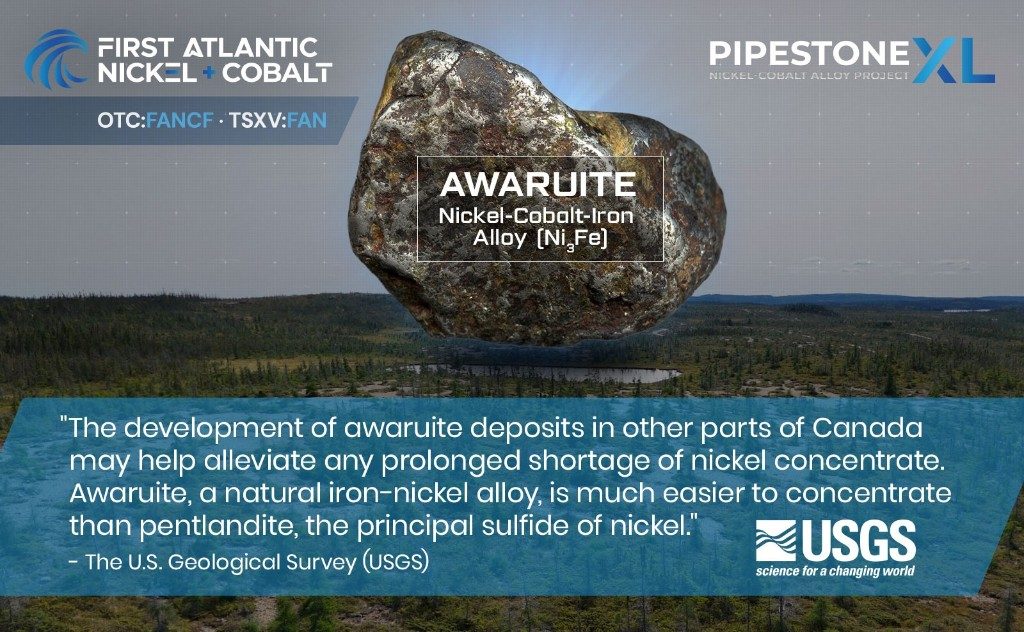

Awaruite is a rare magnetic alloy and one of the highest-grade nickel-cobalt minerals on Earth — approximately 77% pure nickel with 21% iron and 1% cobalt, with no chemical impurities.[18] Because it's naturally magnetic, it can be concentrated using magnetic separator drums — the same proven technology used in Minnesota's Mesabi Iron Range and Labrador's iron mines for over a century.

Awaruite (Ni₃Fe) can be concentrated right at the mine into a sulfur-free concentrate of up to 60% nickel and ~1% cobalt, with cobalt carried naturally within the awaruite alloy itself. This unlocks domestic U.S. refining of battery-grade nickel sulphate (NiSO₄), the pCAM feedstock used for EV cathodes. Nickel sulphate is the emerald-green crystalline salt that cathode precursor plants combine with either manganese (NMC) or aluminum (NCA) to build the active material inside lithium-ion batteries. These are the same battery chemistries Tesla, Panasonic and LG manufacture in the United States.

Section 45X of the U.S. Advanced Manufacturing Production Credit pays domestic producers 10% of production costs for critical minerals refined in the United States, including nickel, plus $35 per kWh for battery cells produced domestically. For nickel, the credit only pays out if the nickel concentrate from the mine is refined into nickel sulphate (or purified to 99%+ purity) within the United States[25], and that is where conventional nickel sulfide or laterite runs into a wall.

To be refined into nickel sulphate, nickel first has to be in a suitable metallic or alloy form. Awaruite is a natural nickel-iron alloy, so it already is. Sulfide nickel is not an alloy. It is chemically bound to sulfur, which must be driven off in a high-temperature smelter first. North American smelting capacity is severely constrained, with no new smelters under construction or permitted, and nickel sourced from Foreign Entities of Concern (FEOC), including China and Chinese-controlled Indonesian processing, disqualifies the end product from 45X eligibility. Awaruite skips the smelter entirely and goes straight into a U.S. nickel refinery to be converted directly into 45X-qualifying nickel sulphate.

Common nickel sulfide ores require smelting that emits toxic SO₂, uses massive amounts of electricity, and risks creating acid mine drainage — nearly impossible to permit or profit from in Western jurisdictions. Laterite ores require high-pressure acid leaching with massive chemical inputs, producing significant volumes of sulfuric acid waste. Awaruite has none of these problems:

| Awaruite (Ni₃Fe) | Sulfide & Laterite Nickel | |

|---|---|---|

| Nickel Grade | ~77% pure nickel — natural alloy | ~25% sulfide; 1–2% laterite |

| Nickel Concentrate Grade | ~60% Nickel, 1% Cobalt. | 1–15% Nickel |

| Mine Site Processing | Simple magnetic separation, flotation | Flotation, Smelting, roasting, or high-pressure acid leaching |

| Secondary Processing — Smelting, HPAL Roasting | Not Required (Awaruite is Pure Metal Alloy). Direct Concentrate shipped. | Required for Sulfide & Laterite Nickel. Additional capital and energy costs required after mining. |

| Electricity Demand | Low | High (Processing — Smelting, Roasting, HPAL) |

| Pollution & Acidic Mine Waste | None | SO₂, acid mine drainage, sulfuric acid waste |

| Tailings | Sulfur-free and inert | Toxic |

| Permitting | Faster — safer environmental footprint | Difficult — toxic waste and tailings |

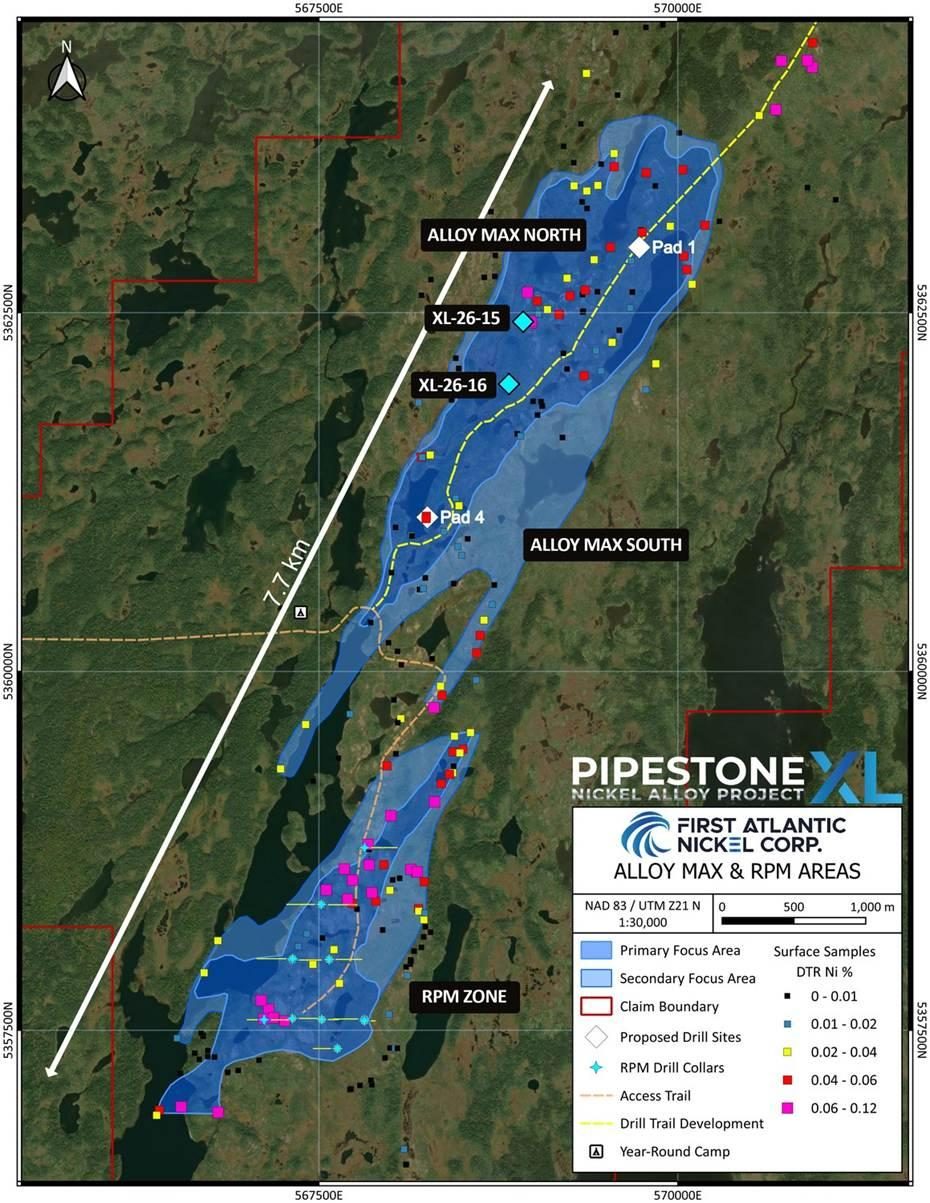

The Pipestone XL Nickel-Cobalt Alloy Project is a 30-kilometer geological system in Newfoundland — a 489-million-year-old ophiolite of ancient ocean crust and mantle thrust onto land along the Appalachian Orogen. The entire 30km belt is enriched in nickel, cobalt, and chromium through serpentinization, a natural process that releases nickel from the rocks to create a nickel-cobalt alloy.

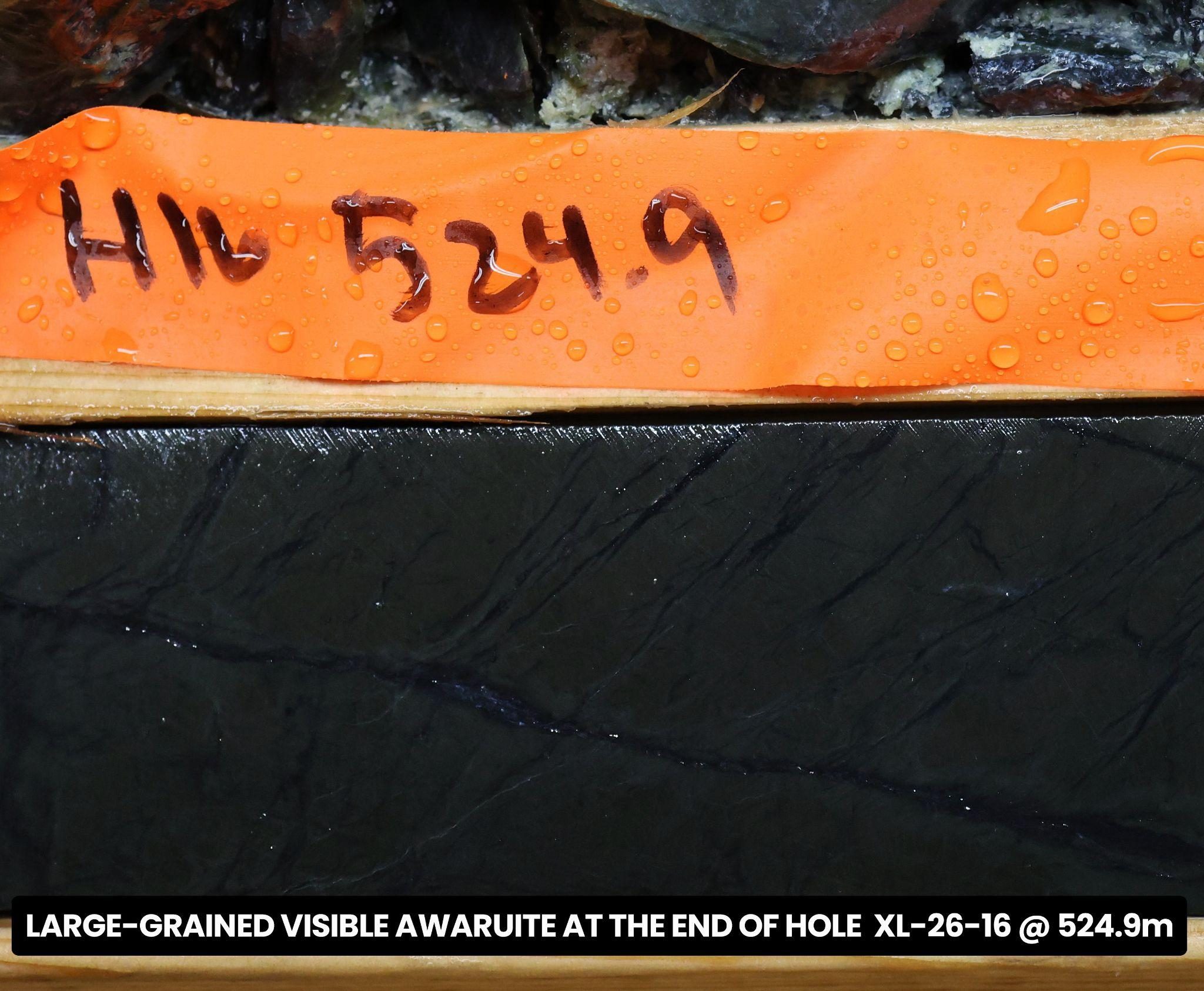

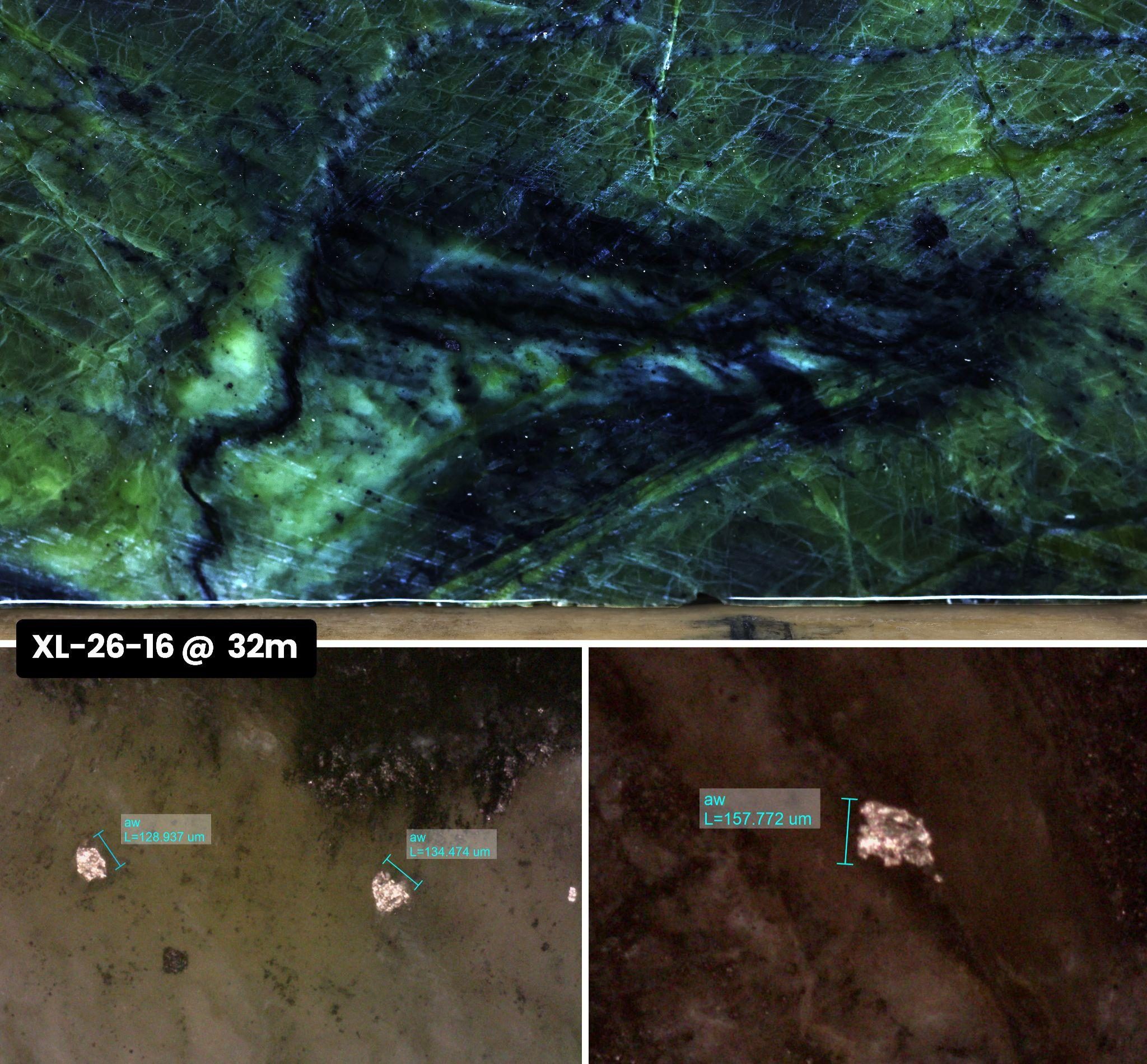

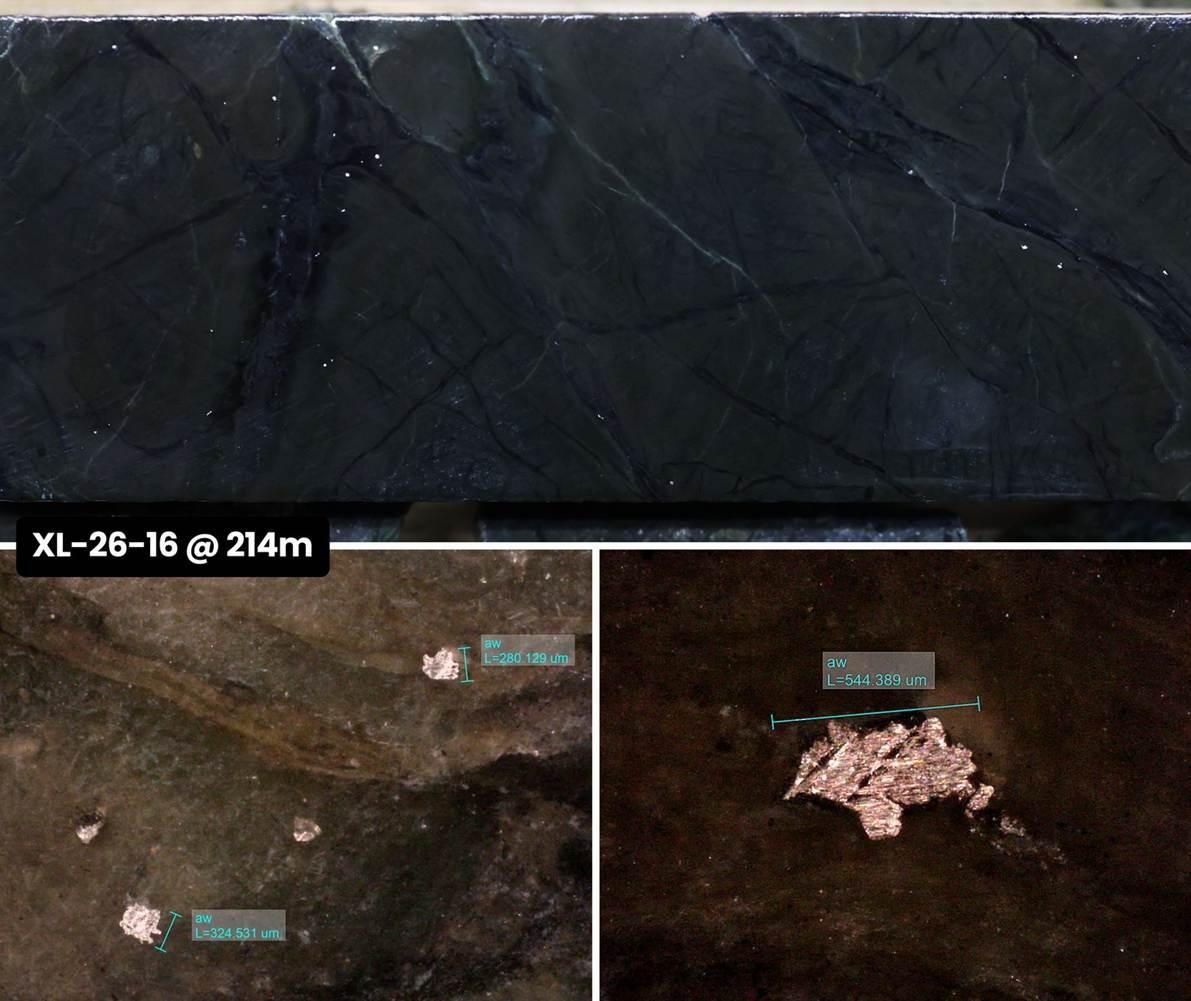

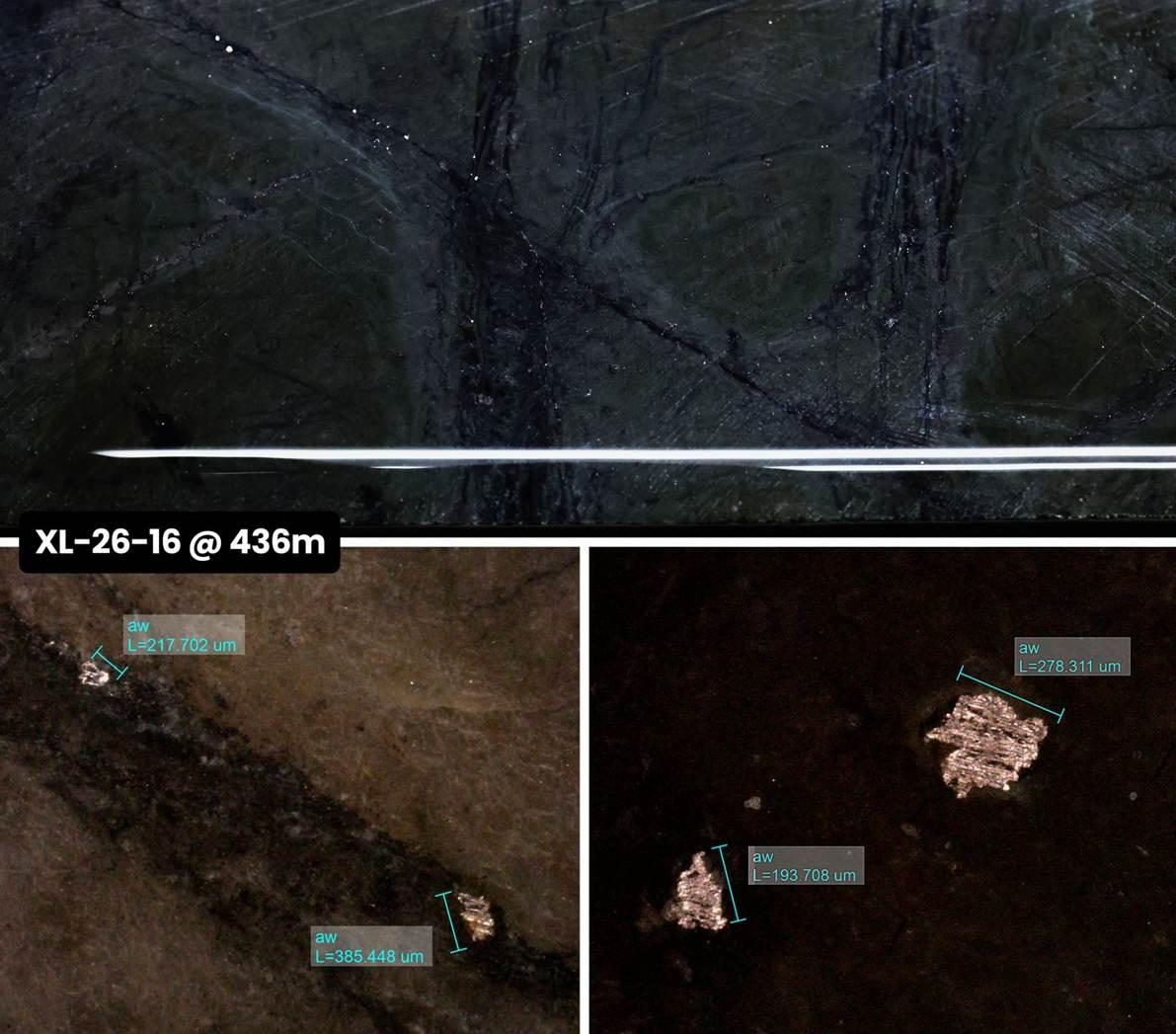

Four discovery zones have been confirmed — RPM Zone, Super Gulp Zone, and Atlantic Lake — where drilling has confirmed awaruite: a magnetically recoverable nickel-cobalt alloy mineralization associated with chromite.

2024: 5 holes drilled with a 100% success rate.

2025: 9 additional holes expanded the RPM Zone to 1.2km strike length and 800m width, with intercepts up to 447 meters.

RPM Zone magnetic concentrates up to 2.35% nickel and 8.17% chromium confirmed.

2026: Discovery of new, larger 4km Alloy Max Zone, located 7km north of the RPM Zone.

Additional metallurgical results and drilling are planned for 2026. First Atlantic owns 100% of this district-scale discovery. The last major nickel-cobalt discovery in Newfoundland, Voisey's Bay, saw shares surge 20-fold before its $4.3 billion acquisition at $41 a share.[20] In 2022, Tesla signed a supply deal with Vale for nickel from Voisey's Bay to supply its North American gigafactories.[21]

The Pipestone XL project is positioned at the intersection of four converging forces: national security, battery demand, smelter-free processing, and a jurisdiction that qualifies as a domestic source under the U.S. Defense Production Act.

First Atlantic Nickel & Cobalt's Ophiolite-X acquisition in the Bay of Islands complex targets geologic hydrogen, carbon capture, and additional critical minerals. Natural springs discharge hydrogen from active serpentinization at costs estimated below the U.S. DOE's $1/kg target, and Memorial University calculates CO₂ storage capacity equivalent to more than 13 years of global emissions. NASA studies the Tablelands massif as a Mars analogue.

Chromium recovery addresses a separate but equally urgent gap: the U.S. has not mined chromium since 1962 and imports 83% of its supply.

"Two Canadian provinces, Saskatchewan and Newfoundland & Labrador, appear in the list of top ten most attractive jurisdictions for mining investment."[22]

— Fraser Institute Annual Survey, 2025 (350 participants, 82 jurisdictions)Newfoundland is a Canadian province located between the United States and Greenland in the Atlantic, and is considered a "domestic source" under Title III of the U.S. Defense Production Act. Of the 46 minerals identified as critical by the U.S., EU, Japan, Australia, UK, and South Korea, Newfoundland and Labrador hosts 31.

The province consistently ranks among the top 10 global mining jurisdictions for geological potential, competitive regulatory environment, and long-term political stability. Hydro rates are among the cheapest in North America. Deep-sea port access enables direct Atlantic shipping to U.S. and European manufacturers. Newfoundland projects are among the fastest to be permitted on the continent.

There are no First Nations land rights issues that have stalled comparable projects elsewhere in Canada. FPX Nickel's Baptiste Project in British Columbia — the only other company to have identified awaruite as a primary resource — has been delayed due to permitting, First Nations opposition and location challenges.

The supply squeeze is already underway. Since September 2025, Indonesia has cut nickel mining quotas more than 30% and piled on new taxes, royalties, and export controls — driving nickel up 35% to $19,138/t — with further policy-driven supply cuts expected in 2026. The DRC has done the same to cobalt, sending prices up 65% to $55,858/t.

These are early signals in a market the IMF projects will grow dramatically through 2040: real prices of nickel, cobalt, and lithium could rise several hundred percent from 2020 levels, with accumulated nickel production value of $4.1 trillion through 2040.[23]

The IEA predicts 60 new nickel mines and 17 new cobalt mines will be required by 2030.[24] Nickel consumption is projected to increase up to 4x by 2040. Tesla CEO Elon Musk has stated the company is moving at "top speed" to reach 1,000 GWh per year of battery production in the U.S. alone, requiring an estimated 750,000 tons of nickel per year — the equivalent of roughly 18 average-size nickel mines. More than 300 gigafactory-type developments are completed, underway, or planned globally.

Washington's race to onshore critical minerals is no longer a talking point. The White House has declared it a national emergency. The Federal Reserve has warned of the economic consequences of nickel import dependence. When the DoD took a major equity stake in MP Materials, Apple invested $500 million and General Motors followed. Nickel and cobalt are next.

First Atlantic Nickel & Cobalt Corp. represents that same category of opportunity — a smelter-free, North American source that feeds directly into U.S. manufacturing without touching Chinese processing infrastructure.

Add $FANCF to Your Watch List — U.S. Brokerages

Add $FAN.V to Your Watch List — Canadian Brokerages

Sources

Disclaimer

This webpage has been prepared and distributed by First Atlantic Nickel & Cobalt Corp. and constitutes a promotional communication. It is provided for informational purposes only and does not constitute financial or investment advice or a recommendation, offer or solicitation to buy or sell any securities. Investing in securities involves risk, including the risk of loss of principal. Past performance is not indicative of future results, and no assurance can be given that any objectives, projections or expectations described on this page will be achieved. Market forecasts cited on this page are third-party views and are inherently uncertain; actual price and demand outcomes may differ materially.

No securities regulator or stock exchange has reviewed or accepts responsibility for its contents. Recipients should conduct their own research and consult qualified investment professionals before making any investment decisions. By reading this communication, you acknowledge and agree that neither First Atlantic Nickel & Cobalt Corp. nor any of its directors, officers, employees, agents, or promoters accepts any liability for any direct or consequential loss or damages arising from reliance on the information contained herein.

Scientific and Technical Information

The scientific and technical information on this page has been reviewed and approved by Adrian Smith, director and the Chief Executive Officer of the Company whom is a qualified person as defined by NI 43-101. The qualified person is a member in good standing of the Professional Engineers and Geoscientists Newfoundland and Labrador (PEGNL) and is a registered professional geoscientist (P.Geo.). Unless otherwise indicated, the technical information on this page is derived from the Company's previously filed disclosure, including news releases available under the Company's profile on SEDAR+.

Forward-Looking Information

This page contains "forward-looking information" within the meaning of applicable Canadian securities laws, including, without limitation, statements regarding: anticipated North American and U.S. demand for nickel, cobalt and chromium; projected supply deficits, import dependence and price trends; the potential strategic importance of the Pipestone XL Project; the potential for awaruite mineralization to support smelter-free or onshore processing; the potential ability of concentrate from the Project to be processed by downstream North American customers; expected metallurgical, recovery, concentrate grade, by-product and processing outcomes; the extent, scale and continuity of mineralization; future exploration, drilling, metallurgical testing and development plans; permitting, environmental, infrastructure and timeline advantages; and potential opportunities relating to chromium, geologic hydrogen and carbon capture. Forward-looking information is often, but not always, identified by words such as "expects," "plans," "targets," "believes," "projects," "potential," "could," "may," "will," "anticipates," and similar expressions.

Forward-looking information on this page is based on a number of material factors and assumptions, including, among other things: the accuracy of current geological, geophysical, geochemical, drilling, sampling, assay and metallurgical data interpretations; the continuation of observed mineralization and metallurgical characteristics; the ability to obtain results from additional drilling and testing consistent with results to date; the availability of financing, personnel, equipment and contractor support; the timely receipt of permits, approvals and access; the availability of infrastructure, processing, refining and transportation alternatives; the continuation of supportive critical mineral, trade and industrial policies in Canada and the United States; and management's current expectations regarding market conditions, demand, pricing and supply chain dynamics for nickel, cobalt and chromium.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those expressed or implied by such forward-looking information. These include, without limitation: exploration results not supporting current interpretations; drilling, sampling, assay, metallurgical or recovery results that differ from results obtained to date; the absence of a mineral resource estimate or economic study demonstrating economic viability; changes in commodity prices, demand forecasts, tariffs, quotas, trade measures or critical mineral policies; the inability to secure financing, permits, social licence, infrastructure, contractors, processing arrangements or offtake relationships on acceptable terms or at all; technical, engineering, processing, scale-up or recovery challenges; cost inflation; environmental and regulatory risks; title, access, weather and operational risks; and general economic, market and capital markets conditions. Readers are cautioned that actual results may differ materially from the forward-looking information on this page, and undue reliance should not be placed on such information.

The forward-looking information on this page is made as of the date of publication of this page, and First Atlantic Nickel & Cobalt Corp. undertakes no obligation to update or revise such information except as required by applicable securities laws.

Readers should review the Company's continuous disclosure filings available on SEDAR+ and should conduct their own independent review before making any investment decision.

Our White Paper on Onshoring the North American Nickel-Cobalt Supply Chain

Now available — enter your email and we’ll send it to you instantly.