TSX-V: FAN

OTCQB: FANCF

$FAN.V

$FAN.V  $FANCF

$FANCF

First Atlantic Nickel & Cobalt Corp. TSX-V: FAN | OTCQB: FANCF

First Atlantic's awaruite discovery in Newfoundland is the largest nickel-cobalt alloy and chromium discovery in the Atlantic in 30 years and bypasses the processing bottlenecks that have been stalling Canadian critical minerals development for decades.

Key Takeaways

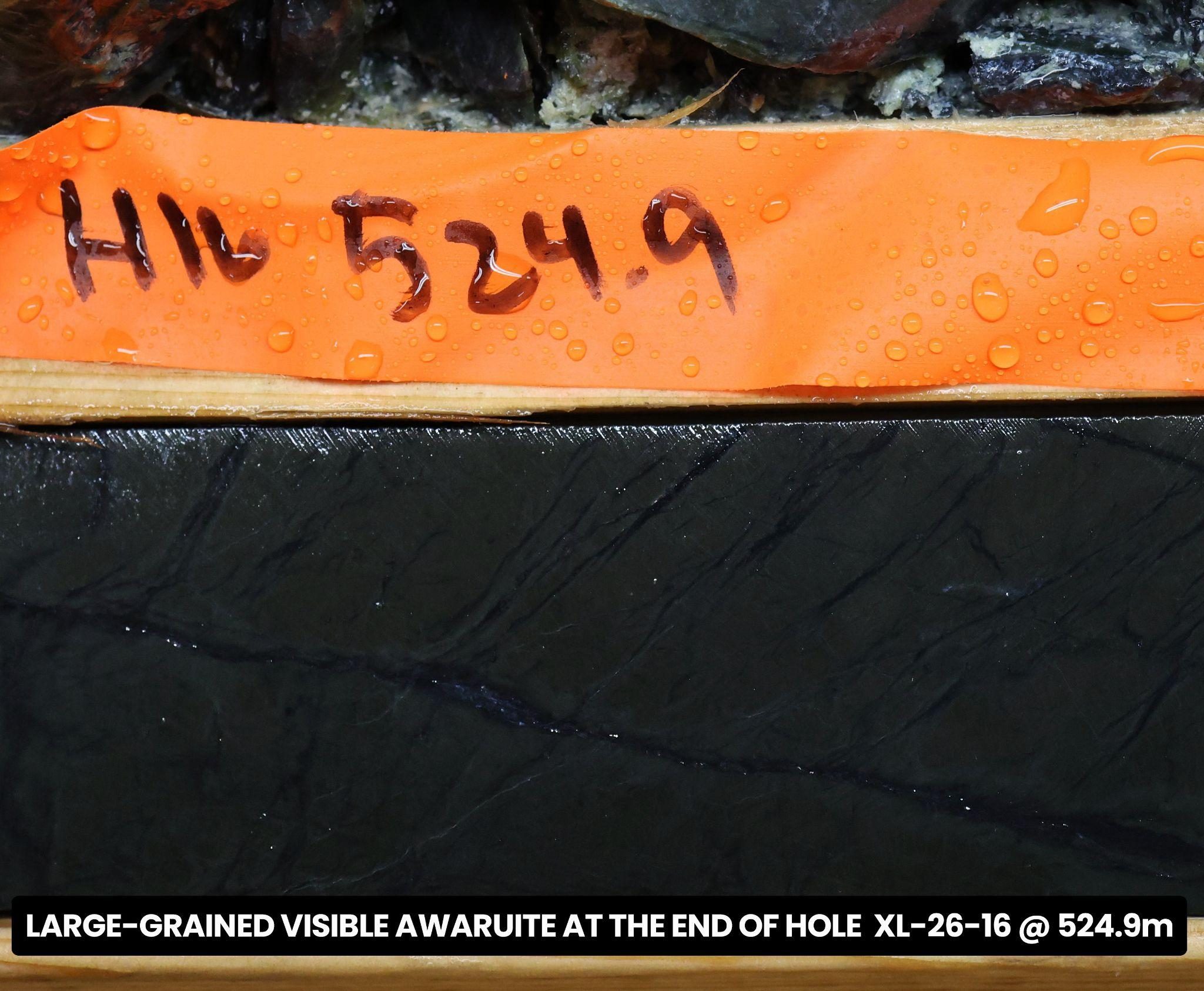

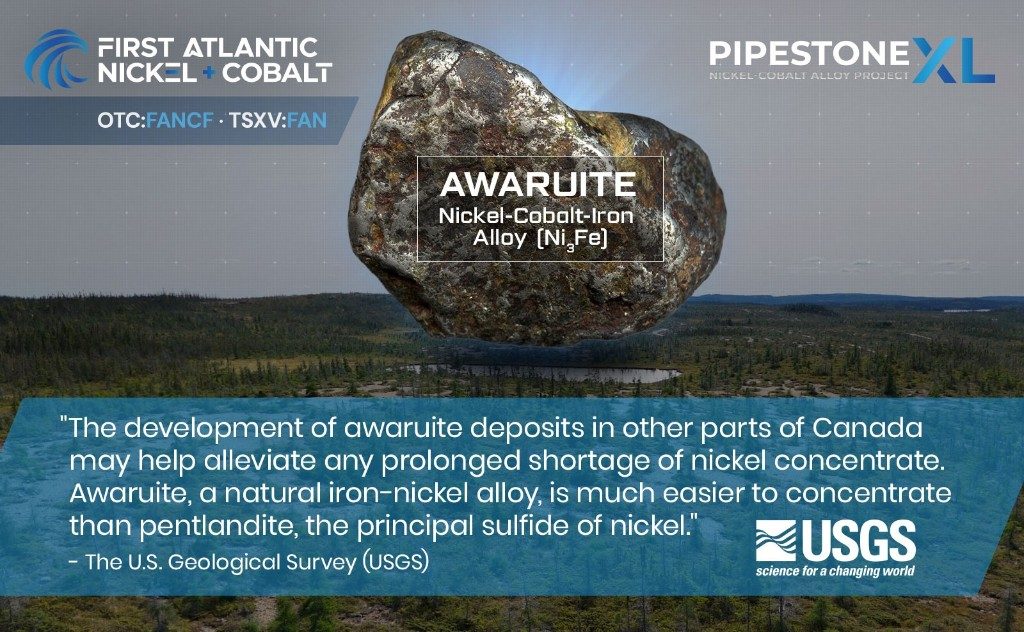

First Atlantic Nickel & Cobalt (TSXV: FAN | OTC: FANCF) has drilled the largest nickel-cobalt alloy and chromium discovery in the Atlantic in 30 years. The last one was Voisey's Bay, acquired for $4.3 billion at $43.50 a share in 1996 (more than $8 billion in today's dollars)[1]. The Pipestone XL discovery hosts awaruite (Ni₃Fe), Earth's rarest naturally magnetic nickel-cobalt alloy, ~77% pure nickel, recoverable through simple magnetic separation. No smelter required.

The timing could not be sharper. The IEA forecasts 60 new nickel mines and 17 cobalt mines needed by 2030, with global nickel consumption potentially rising fourfold by 2040[2]. Yet the U.S. holds just 1% of global nickel reserves[3], Japan imports over 90% of its critical minerals, and Europe's largest nickel refinery still runs on Russian feedstock.

"The IMF projects that real prices of nickel, cobalt and lithium would rise several hundred percent from 2020 levels... total accumulated production value from 2021–2040 reaching $4.1 trillion for nickel, $1.6 trillion for cobalt, across all four critical energy transition metals, over $13 trillion, rivaling the total value of crude oil production."[4]

— International Monetary FundMeanwhile, Indonesia supplies more than 60% of the world's nickel, and Chinese state-backed companies have invested an estimated $65 billion to control 90% of its industry[5]. Indonesia has now banned raw ore exports, added taxes and royalties, and cut mining quotas more than 30%, driving nickel prices up 35% to $19,138 per metric ton. The DRC has done the same to cobalt, pushing prices up 65%[6]. A conflict near the Strait of Hormuz is now threatening the sulfuric acid supply that Indonesian laterite processing depends on. The risks are no longer theoretical.

Canada has signed critical minerals agreements with the EU, Japan, South Korea, and the United States[7], and every one of them needs nickel and cobalt from a source not controlled by China. But anyone who has followed Canadian critical minerals long enough knows the pattern. In February 2026, the Royal Bank of Canada called it out as a "mine and ship jurisdiction."

Promising deposit. Right geology. Wrong jurisdiction. Limited processing capability.

Pipestone XL breaks that pattern. Located in Newfoundland, Canada's top-ranked mining jurisdiction[8], with road access, grid power, and no smelter required, the project is positioned to bypass the midstream processing bottleneck that has stalled Canadian nickel development for a decade and to supply allied-nation economies with a secure, Canadian-mined source of nickel and cobalt for advanced manufacturing and the energy transition.

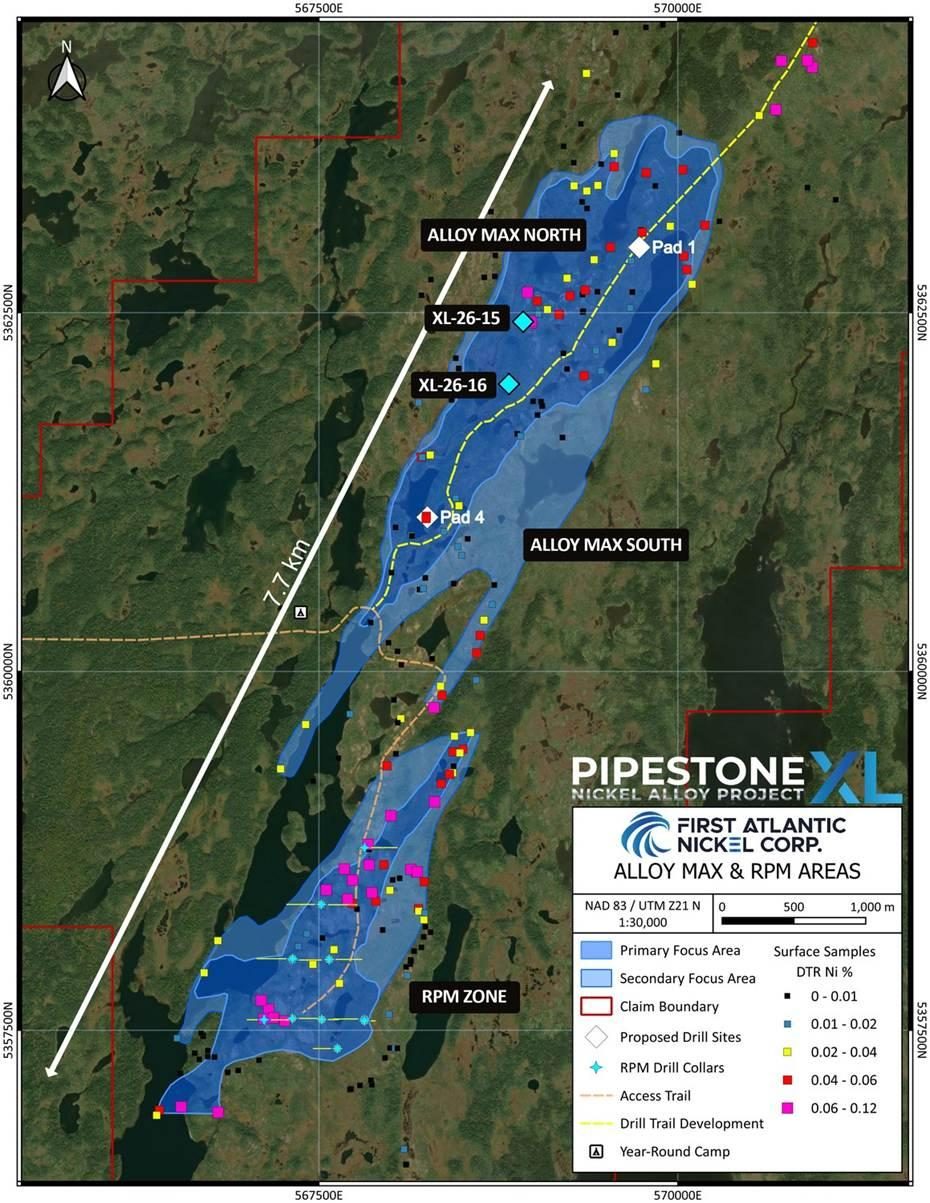

The 30-kilometer district already hosts two large-scale awaruite target areas: the RPM Zone, where drilling has confirmed nickel-cobalt alloy mineralization over 1.2 km by 800 m, and the newly discovered Alloy Max Zone, 7 km to the north, spanning an initial 4 km by 1.2 km target area, roughly four times RPM's footprint and, based on early geophysical analysis, potentially larger still.

Because awaruite is concentrated through simple magnetic separation rather than smelting, the process is expected to use less energy, produce no sulfur dioxide emissions, and generate non-toxic, non-acid-generating tailings, a sustainable, low-carbon pathway aligned with Canada's clean economy goals.

Pipestone XL also carries additional upside beyond nickel and cobalt. The 30-kilometer district is also enriched in chromium, with magnetic concentrates at the RPM Zone confirming up to 8.17% chromium, and the project’s ultramafic host rocks naturally contain brucite and serpentine minerals that react with CO₂ and water, opening long-term opportunities in stimulated geologic hydrogen generation and mineral carbon capture.

First Atlantic Nickel & Cobalt Corp. (TSXV: FAN | OTC: FANCF) could be one of the most strategic and valuable critical mineral discoveries in the Western Hemisphere. Pipestone XL has the potential to provide a large-scale, long-life source of domestic nickel-cobalt alloy concentrate that connects the full critical mineral value chain, from upstream mining and domestic processing straight into downstream U.S. and Canadian manufacturing, capable of moving directly from mine to EV battery refinery, bypassing the smelter entirely. The project has the potential to anchor new manufacturing industries in Canada, from stainless steel and specialty alloys to EV battery manufacturing, keeping processing, jobs, and economic value on Canadian soil and supporting Canadian sovereignty over its own critical minerals.

Canada has no shortage of world-class critical mineral deposits. Moving them from discovery to production is where the story usually falls apart. And the rest of the world has been paying attention.

Canada has signed critical minerals agreements with every major allied economy. All of them need nickel. None of them has enough supply locked up.

European Union

European Union

Signed its first-ever critical raw materials partnership with Canada. Largest EU nickel refinery runs on 94% Russian feedstock.

Japan

Japan

Signed a comprehensive strategic partnership with Canada in March 2026. Imports 91% of its critical minerals.

Every major allied economy is asking Canada for nickel, and we're not delivering.

Canada's critical minerals sector has been stalled by the same two forces for decades.

Red tape. Permitting across most Canadian provinces takes years. Environmental review, capital requirements, and First Nations consultation processes have stopped more than one viable project before it ever got started.

Limited domestic processing capacity. Canada has built no new nickel smelters in decades as it's held back by prohibitive costs, permitting delays, environmental regulations, and rising energy demands. Even when ore comes out of the ground, there is nowhere to process it. It gets shipped offshore and foreign operators take over from there.

In March 2026, the House of Commons Standing Committee on National Defence heard testimony that made headlines across the country. Most critical minerals mined in Canada leave the country for processing, primarily to China. Copper from British Columbia. Lithium from Quebec. Nickel from northern Quebec's Nunavik mine, owned by a Chinese company since 2009, shipped directly overseas for processing.

"The real strategic vulnerability today is not our geology; it is our processing capacity and supply chain dependence."

— Dr. Nadia Mykytczuk, Executive Director, Goodman School of Mines, Laurentian University. Testimony to the House of Commons Standing Committee on National Defence.RBC's February 2026 "Mine & Refine" report laid out how deep the problem runs. China controls 70% of global refining for 19 of the world's 20 most critical minerals[14]. Between 2005 and 2012, more than $119 billion in Canadian base metals and steel assets transferred to foreign ownership. Canada committed $55 billion to attract EV manufacturers without attaching domestic sourcing conditions.

Canada's processing infrastructure has been disappearing in real time, due to tighter environmental standards and rising electricity costs. Thompson, Manitoba's nickel smelter, shut down in 2018[15]. Only two small nickel smelters remain in Sudbury[16]. Glencore's Horne facility in Quebec, Canada's last remaining copper smelter, suspended $1 billion in planned investments in February 2026 after a dispute over emissions regulations. And building replacements isn't realistic. New metal smelters can cost $5 to $9 billion, take a decade or more to permit, and the last five Western-built smelters had cost overruns averaging 70 to 300%. Two have already shut down. One was written off entirely.

During World War II, Canada produced 95% of all Allied nickel and 40% of Allied aluminum. Today, it ships raw ore to Beijing.

"Canada's lack of mineral processing capabilities is a defence vulnerability."

— House of Commons Standing Committee on National Defence, March 2026Northern Ontario's Ring of Fire holds an estimated $60 billion in critical minerals. Discovered in 2007, the deposit has yet to see a single shovel in the ground.

The reasons are structural. It sits in one of the most remote areas of the province, with no road access, no grid power, and no rail connections. Bringing that infrastructure to the site would cost multiples of what it costs to build the mine itself. First Nations land rights remain unresolved, with multiple lawsuits pending and not all rights-holders having consented. And no smelter exists to process what comes out of the ground. Building one to North American standard costs up to $8 billion USD.

Cliffs Natural Resources learned this firsthand. In 2011, Bill Boor, Cliffs' SVP, stated plainly: "At current provincial power rates, there isn't a location in Ontario that is economically viable for Cliffs to build the FPF." So they walked, and the economics haven't improved since. The Ontarians for a Just Accountable Mineral Strategy put it directly: "Without taxpayer investment exceeding $2 billion, the Eagle's Nest Mine is not viable" and "a ferrochrome smelter is an enormous consumer of electricity and would also have to be heavily subsidized."

The Ring of Fire is an infrastructure, energy, and permitting problem. And it's exactly the kind of problem that Pipestone XL doesn't have.

First Atlantic Nickel & Cobalt Corp. (OTC: FANCF | TSX-V: FAN) has drilled the first major awaruite discovery since the USGS identified it as a solution to nickel shortages in 2012[17]. It's in the one Canadian province where every infrastructure obstacle that has killed other projects simply doesn't exist.

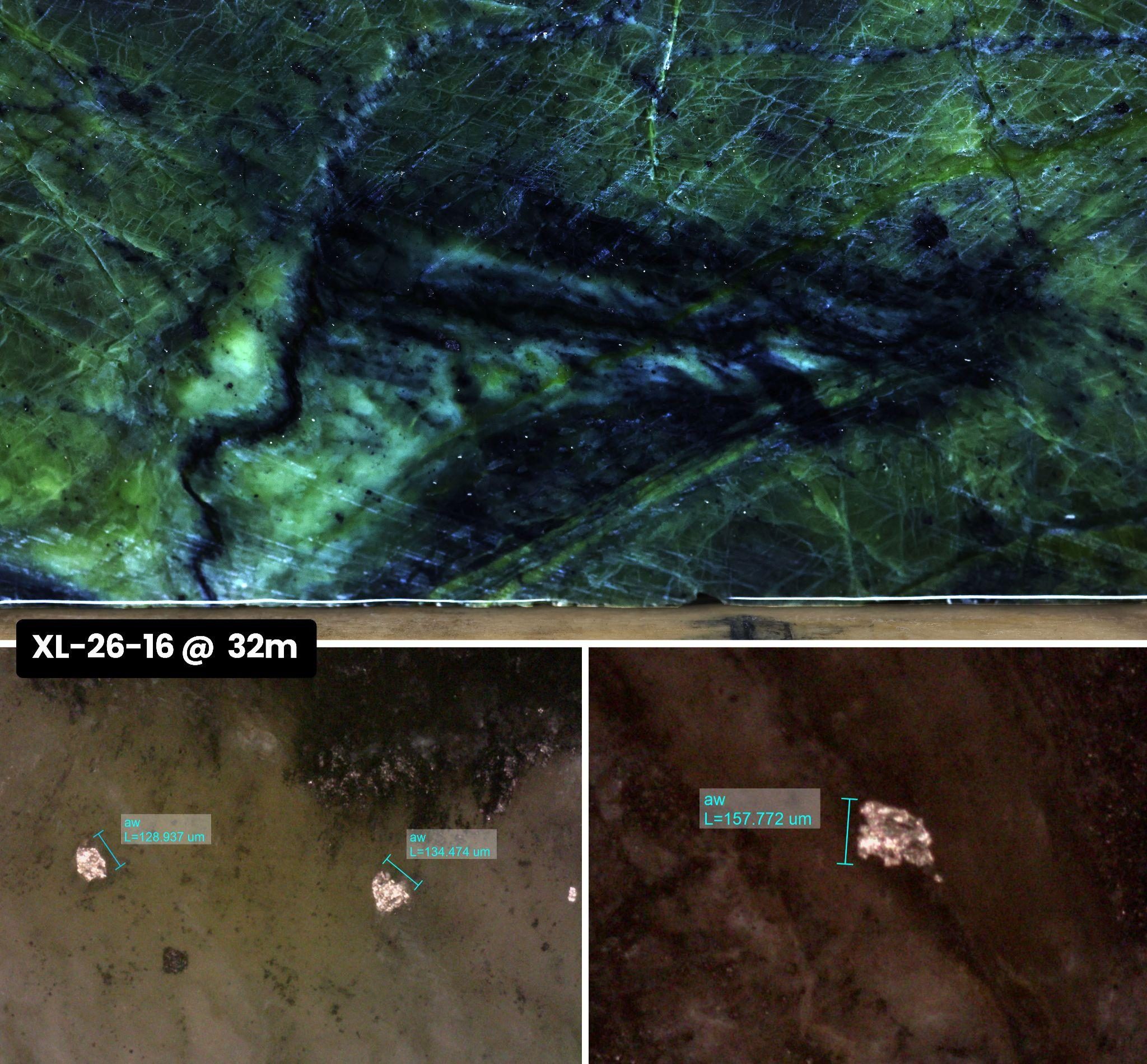

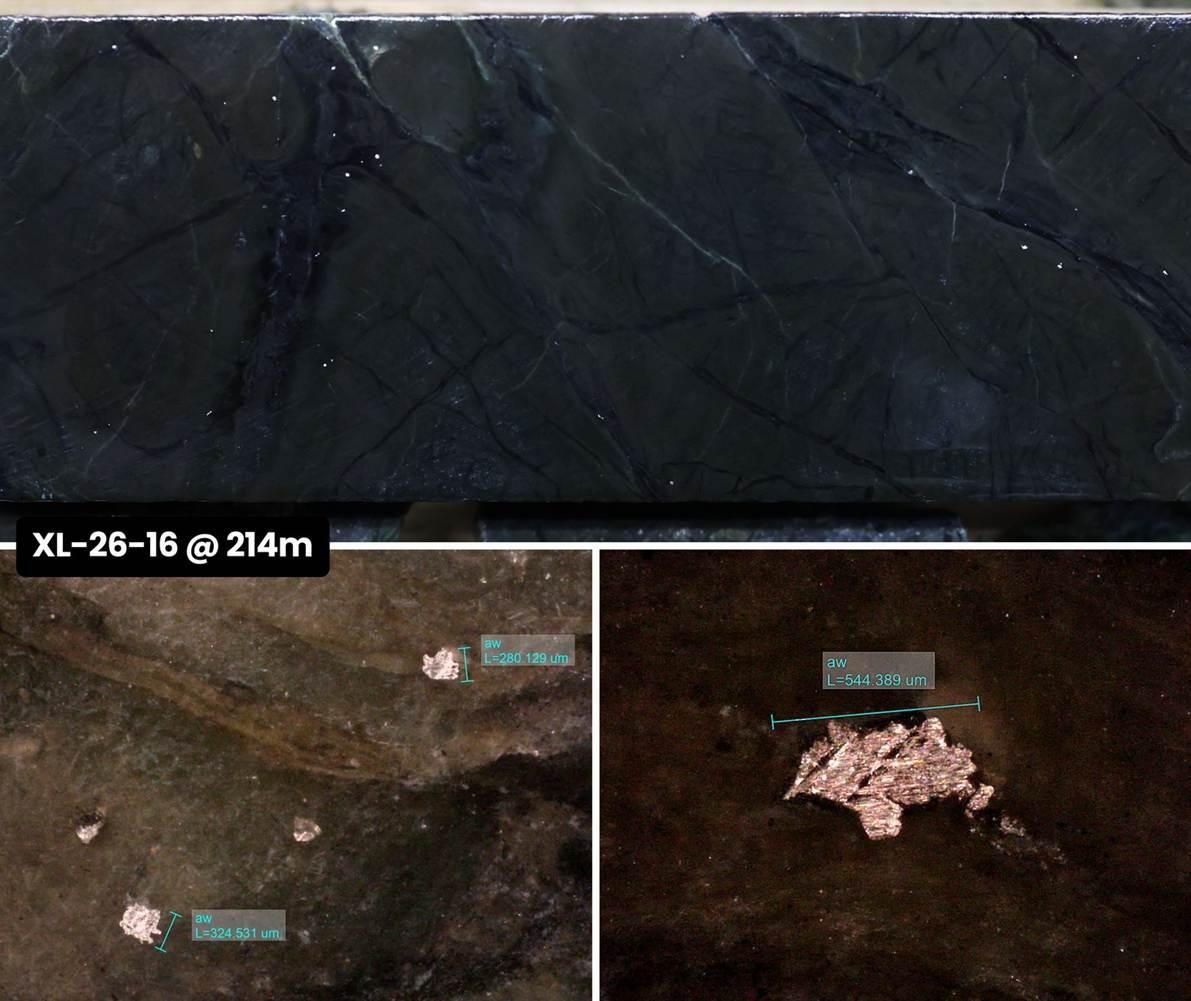

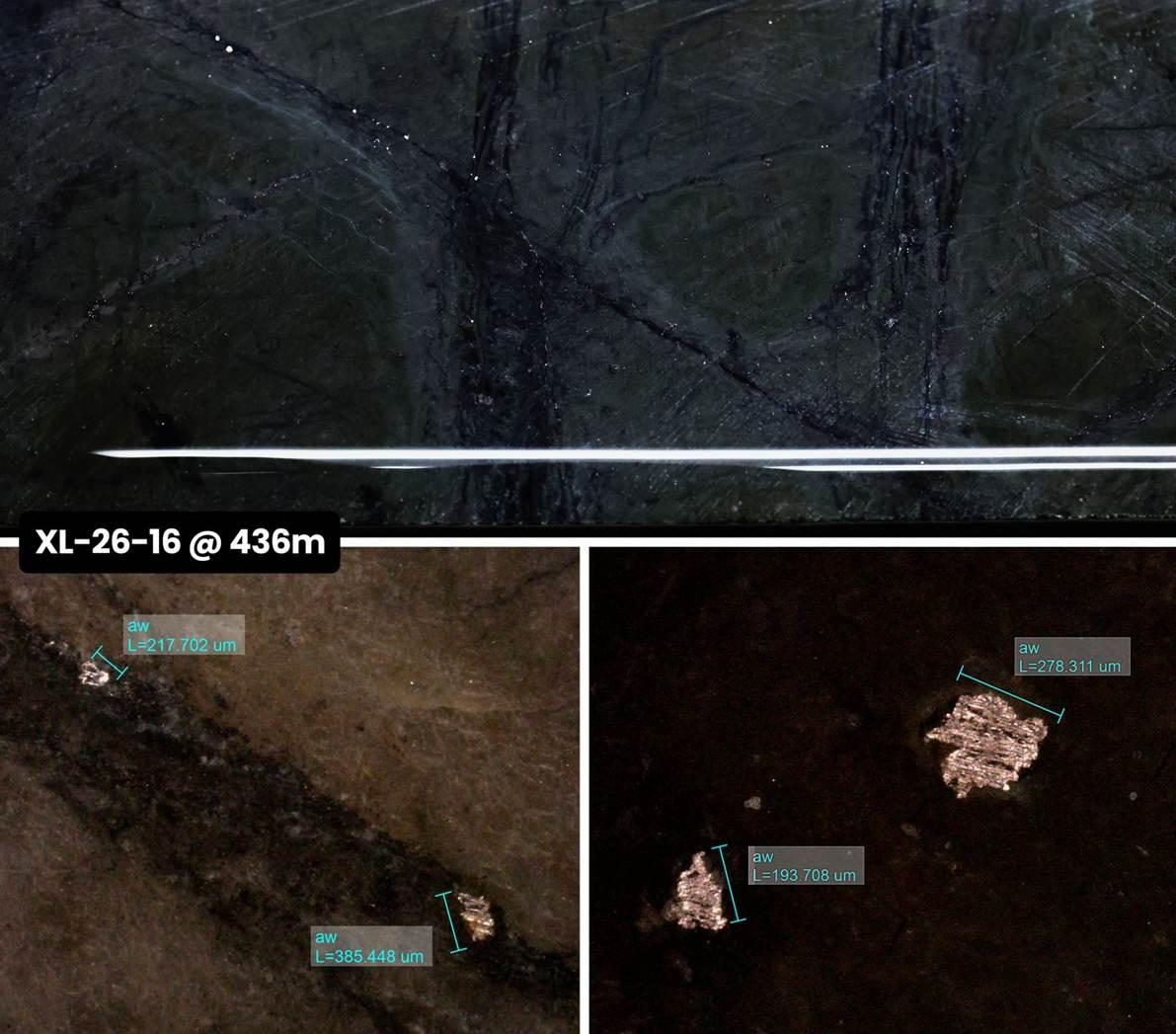

Awaruite (Ni₃Fe) is a naturally occurring magnetic nickel-iron-cobalt alloy — approximately 77% pure nickel with 21% iron and 1% cobalt[18]. It's not a sulphide. It doesn't behave like one. And it doesn't need to be processed like one.

Because awaruite is magnetic, it can be concentrated using magnetic separator drums — the same proven technology that Minnesota's Mesabi Iron Range and Labrador's iron mines have used for over a century.

Awaruite (Ni₃Fe) can be concentrated right at the mine into a sulfur-free concentrate of up to 60% nickel and ~1% cobalt[19], with cobalt carried naturally within the awaruite alloy itself. This unlocks domestic U.S. refining of battery-grade nickel sulphate (NiSO₄), the pCAM feedstock used for EV cathodes. Nickel sulphate is the emerald-green crystalline salt that cathode precursor plants combine with either manganese (NMC) or aluminum (NCA) to build the active material inside lithium-ion batteries. These are the same battery chemistries Tesla, Panasonic and LG manufacture in the United States.

Section 45X of the U.S. Advanced Manufacturing Production Credit pays domestic producers 10% of production costs for critical minerals refined in the United States, including nickel, plus $35 per kWh for battery cells produced domestically. For nickel, the credit only pays out if the nickel concentrate from the mine is refined into nickel sulphate (or purified to 99%+ purity) within the United States[20], and that is where conventional nickel sulfide or laterite runs into a wall.

To be refined into nickel sulphate, nickel first has to be in a suitable metallic or alloy form. Awaruite is a natural nickel-iron alloy, so it already is. Sulfide nickel is not an alloy. It is chemically bound to sulfur, which must be driven off in a high-temperature smelter first. North American smelting capacity is severely constrained, with no new smelters under construction or permitted, and nickel sourced from Foreign Entities of Concern (FEOC), including China and Chinese-controlled Indonesian processing, disqualifies the end product from 45X eligibility. Awaruite skips the smelter entirely and goes straight into a U.S. nickel refinery to be converted directly into 45X-qualifying nickel sulphate.

No smelter. No roasting. No sulphur dioxide emissions. No acid mine drainage.

That isn't a marginal improvement. A conventional nickel smelter costs $5 to $9 billion and takes a decade or more to permit and build. The last five Western-built smelters had cost overruns averaging 70–300%. Two have been shut down. One was written to zero. Awaruite bypasses all of it.

| Awaruite (Ni₃Fe) | Sulfide & Laterite Nickel | |

|---|---|---|

| Nickel Grade | ~77% pure nickel — natural alloy | ~25% sulfide; 1–2% laterite |

| Nickel Concentrate Grade | ~60% Nickel, 1% Cobalt. | 1–15% Nickel |

| Mine Site Processing | Simple magnetic separation, flotation | Flotation, Smelting, roasting, or high-pressure acid leaching |

| Secondary Processing — Smelting, HPAL Roasting | Not Required (Awaruite is Pure Metal Alloy). Direct Concentrate shipped. | Required for Sulfide & Laterite Nickel. Additional capital and energy costs required after mining. |

| Electricity Demand | Low | High (Processing — Smelting, Roasting, HPAL) |

| Pollution & Acidic Mine Waste | None | SO₂, acid mine drainage, sulfuric acid waste |

| Tailings | Sulfur-free and inert | Toxic |

| Permitting | Faster — safer environmental footprint | Difficult — toxic waste and tailings |

The Pipestone XL Nickel-Cobalt Alloy Project is a 30-kilometer geological system in Newfoundland — a 489-million-year-old ophiolite of ancient ocean crust and mantle thrust onto land along the Appalachian Orogen. The entire 30km belt is enriched in nickel-cobalt, and chromium through serpentinization, a natural process that releases nickel from the rocks to create a nickel-cobalt alloy.

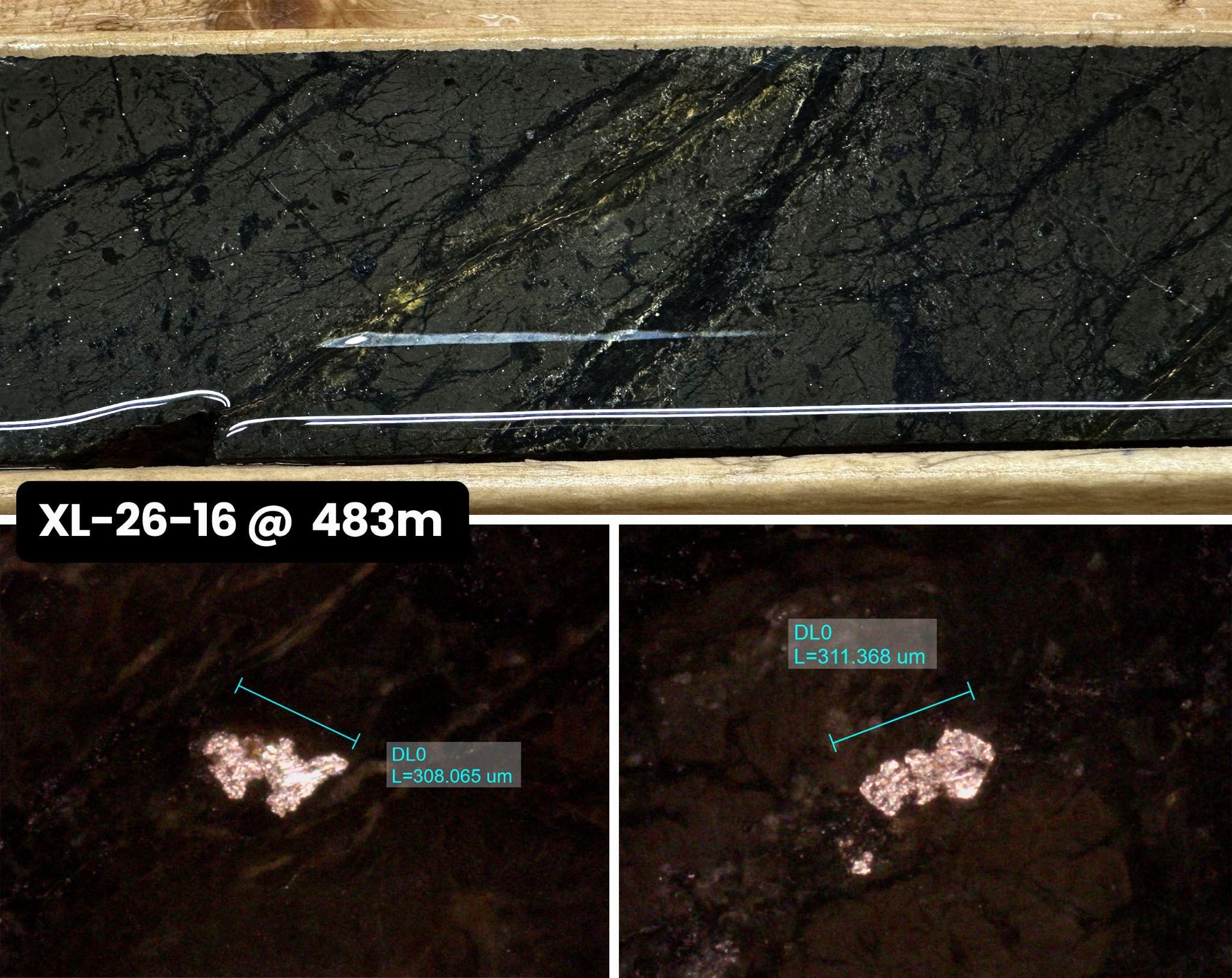

Four discovery zones have been confirmed — RPM Zone, Super Gulp Zone, Atlantic Lake, and the Alloy Max Zone — where drilling has confirmed awaruite: a magnetically recoverable nickel-cobalt alloy mineralization associated with chromite. The Alloy Max Zone, announced in March 2026, extends 7 km north from the RPM Zone.

2024: 5 holes drilled with a 100% success rate.

2025: 9 additional holes expanded the RPM Zone to 1.2km strike length and 800m width, with intercepts up to 447 meters.

RPM Zone magnetic concentrates up to 2.35% nickel and 8.17% chromium confirmed.

2026: Discovery of new, larger 4km Alloy Max Zone, located 7km north of the RPM Zone.

First Atlantic holds 100% of an entire 30-kilometer district. A system this size has the potential to support multiple large open pits across a single geological system — the kind of scale that defines a major mining district.

There is also a chromium story here that most investors haven't caught yet. The United States hasn't mined chromium since 1961[21]. Microprobe analysis at First Atlantic's RPM Zone has confirmed that the chromium is hosted in chromite grading 60.2% Cr₂O₃ — a high-grade chromite by any measure. The Company is now evaluating potential metallurgical processes to separate, concentrate, and process that chromite for stainless steel and superalloy feedstock.

The last major nickel-cobalt discovery in Newfoundland, Voisey's Bay, saw shares surge 20-fold before its $4.3 billion acquisition at $41 a share.[1] In 2022, Tesla signed a supply deal with Vale for nickel from Voisey's Bay to supply its North American gigafactories.[22]

The Pipestone XL project is positioned at the intersection of four converging forces: national security, battery demand, smelter-free processing, and a jurisdiction that qualifies as a domestic source under the U.S. Defense Production Act.

The supply squeeze is already underway. Since September 2025, Indonesia has cut nickel mining quotas more than 30% and piled on new taxes, royalties, and export controls — driving nickel up 35% to $19,138/t. Indonesia slashed RKAB quotas by 34% for 2026, down to roughly 260 million tonnes against smelter demand of 340 to 350 million tonnes — an ore gap exceeding 100 million tonnes. The world's largest nickel mine, Weda Bay, was cut 71%. On March 25, 2026, President Prabowo approved export tariffs on nickel products. The DRC has done the same to cobalt, sending prices up 65% to $55,858/t.

There is now a third pressure point. The Iran conflict and the closure of the Strait of Hormuz have cut off 75% of Indonesia's sulfur imports. Sulfuric acid represents up to 41% of HPAL MHP production costs — the single largest input. Indonesian plants hold only one to two months of sulfur inventory. MHP production already fell 18.6% in March. If the situation worsens, that 30–40% cost increase will flow directly into the price of Indonesian nickel.

These are structural shifts in the world's dominant nickel supply chain, happening simultaneously.

The IMF projects nickel and cobalt prices could rise by several hundred percent through 2040, with accumulated nickel production value reaching $4.1 trillion.[4] The IEA forecasts that 60 new nickel mines will be needed by 2030[23]. The mines don't exist yet, but the demand does.

When the right Canadian nickel deposit surfaces, serious money follows. Lion One was acquired for $6.8 billion USD in 2007. Cosmos shareholders watched their shares rise 58 times before a $3.1 billion USD deal closed. Diamond Fields and Sirius were acquired at significant premiums. Voisey's Bay, the last major nickel-cobalt discovery in Newfoundland, sold for $4.3 billion at $41 per share, with shares up 20-fold going into the deal. Tesla signed a supply agreement with Vale in 2022 to secure Voisey's Bay nickel for its North American gigafactories.[22]

But not all nickel is created equal. Canada Nickel's Crawford project in Ontario is nickel sulphide, which requires smelting before refining. Two small smelters remain in Canada. That means shipping concentrate overseas or spending billions on infrastructure that doesn't exist. Awaruite skips the smelter entirely, moving from the ground to refinery-ready concentrate through magnetic separation alone.

Pipestone XL is the first discovery of comparable scale in that district in 30 years. The sector looks different now than it did in 1996. The demand is greater, and the supply gap is wider. And there is no Voisey's Bay sitting in reserve waiting to fill it.

Canada has what the world is competing for. The sector's problems are real and well-documented. Pipestone XL was built around every one of them. Newfoundland. No smelter required. Thirty years since the last discovery of this scale in this district.

The race for critical minerals is already underway. First Atlantic is already in position.

$FANCF $FAN.V

Add $FAN.V to Your Watch List — Canadian Brokerages

Add $FANCF to Your Watch List — U.S. Brokerages

Sources

Disclaimer

This webpage has been prepared and distributed by First Atlantic Nickel & Cobalt Corp. and constitutes a promotional communication. It is provided for informational purposes only and does not constitute financial or investment advice or a recommendation, offer or solicitation to buy or sell any securities. Investing in securities involves risk, including the risk of loss of principal. Past performance is not indicative of future results, and no assurance can be given that any objectives, projections or expectations described on this page will be achieved. Market forecasts cited on this page are third-party views and are inherently uncertain; actual price and demand outcomes may differ materially.

No securities regulator or stock exchange has reviewed or accepts responsibility for its contents. Recipients should conduct their own research and consult qualified investment professionals before making any investment decisions. By reading this communication, you acknowledge and agree that neither First Atlantic Nickel & Cobalt Corp. nor any of its directors, officers, employees, agents, or promoters accepts any liability for any direct or consequential loss or damages arising from reliance on the information contained herein.

Scientific and Technical Information

The scientific and technical information on this page has been reviewed and approved by Adrian Smith, director and the Chief Executive Officer of the Company whom is a qualified person as defined by NI 43-101. The qualified person is a member in good standing of the Professional Engineers and Geoscientists Newfoundland and Labrador (PEGNL) and is a registered professional geoscientist (P.Geo.). Unless otherwise indicated, the technical information on this page is derived from the Company's previously filed disclosure, including news releases available under the Company's profile on SEDAR+.

Forward-Looking Information

This page contains "forward-looking information" within the meaning of applicable Canadian securities laws, including, without limitation, statements regarding: anticipated North American and U.S. demand for nickel, cobalt and chromium; projected supply deficits, import dependence and price trends; the potential strategic importance of the Pipestone XL Project; the potential for awaruite mineralization to support smelter-free or onshore processing; the potential ability of concentrate from the Project to be processed by downstream North American customers; expected metallurgical, recovery, concentrate grade, by-product and processing outcomes; the extent, scale and continuity of mineralization; future exploration, drilling, metallurgical testing and development plans; permitting, environmental, infrastructure and timeline advantages; and potential opportunities relating to chromium, geologic hydrogen and carbon capture. Forward-looking information is often, but not always, identified by words such as "expects," "plans," "targets," "believes," "projects," "potential," "could," "may," "will," "anticipates," and similar expressions.

Forward-looking information on this page is based on a number of material factors and assumptions, including, among other things: the accuracy of current geological, geophysical, geochemical, drilling, sampling, assay and metallurgical data interpretations; the continuation of observed mineralization and metallurgical characteristics; the ability to obtain results from additional drilling and testing consistent with results to date; the availability of financing, personnel, equipment and contractor support; the timely receipt of permits, approvals and access; the availability of infrastructure, processing, refining and transportation alternatives; the continuation of supportive critical mineral, trade and industrial policies in Canada and the United States; and management's current expectations regarding market conditions, demand, pricing and supply chain dynamics for nickel, cobalt and chromium.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those expressed or implied by such forward-looking information. These include, without limitation: exploration results not supporting current interpretations; drilling, sampling, assay, metallurgical or recovery results that differ from results obtained to date; the absence of a mineral resource estimate or economic study demonstrating economic viability; changes in commodity prices, demand forecasts, tariffs, quotas, trade measures or critical mineral policies; the inability to secure financing, permits, social licence, infrastructure, contractors, processing arrangements or offtake relationships on acceptable terms or at all; technical, engineering, processing, scale-up or recovery challenges; cost inflation; environmental and regulatory risks; title, access, weather and operational risks; and general economic, market and capital markets conditions. Readers are cautioned that actual results may differ materially from the forward-looking information on this page, and undue reliance should not be placed on such information.

The forward-looking information on this page is made as of the date of publication of this page, and First Atlantic Nickel & Cobalt Corp. undertakes no obligation to update or revise such information except as required by applicable securities laws.

Readers should review the Company's continuous disclosure filings available on SEDAR+ and should conduct their own independent review before making any investment decision.

Our White Paper on Onshoring the North American Nickel-Cobalt Supply Chain

Now available — enter your email and we’ll send it to you instantly.

South Korea

South Korea United States

United States